THE ECONOMIC OUTLOOK IN THE CORONAVIRUS PANDEMIC

EXECUTIVE SUMMARY

Click to share

(1) The outbreak of the novel coronavirus (SARS-CoV-2) presents a significant and unprecedented challenge for the entire world. Since it was first detected in China in December 2019, the virus has spread across the globe. In efforts to contain the virus, many countries have introduced rigorous public health measures that significantly limit social contact. The purpose of these measures is to slow the spread of the virus and avoid overwhelming the health systems. At present, it is difficult to say how long the public health measures will need to remain in place and when society will return to normality.

1. Economic impacts

(2) The public health measures are associated with significant economic impacts worldwide. In this Special Report, the German Council of Economic Experts (GCEE) analyses these impacts and discusses suitable economic policy measures to tackle the crisis. In this context, the degree of uncertainty surrounding the future development is currently very high because data is scarce for the brief span of time since the crisis began and because of the exceptional circumstances. The GCEE therefore presents three scenarios for the German economy in 2020 and 2021. These are based on different assumptions regarding the scale and duration of the restrictions as a result of the virus and the speed of the subsequent recovery.

(3) In the baseline scenario – the most likely scenario given currently available information – the GCEE assumes that the economic situation will normalise over the summer, similar to the pattern emerging in China. In this case, GDP would grow by –2.8 % in 2020. In 2021, catch-up effects and a large carry-over effect could drive growth to 3.7 %.

(4) One risk scenario (pronounced V) estimates the economic consequences that could result if there was widespread stoppage of production or if the restrictive measures remained in place longer than currently planned. In this case, economic output in the second quarter could be up to 10 % lower than the current level. The sharper downturn in the first half year of 2020 would result in a drop in GDP of –5.4 % on an annual average. As in the baseline scenario, catch-up effects could, however, ensure a return to economic output that is close to potential as the year progresses, as suggested in the baseline scenario. In 2021, the economy would then grow by 4.9 %; the large carry-over effect of 1.1 percentage points must be taken into consideration here, however.

(5) If the measures to contain the coronavirus last beyond the summer, this will delay economic recovery until 2021. In this risk scenario (long U), the policy measures taken may not be enough to prevent far-reaching damage to the economy resulting from bankruptcies and layoffs. Deteriorating financing conditions and increased and entrenched uncertainty could also curb investment and result in restrained household spending. Ultimately in such a scenario there is a risk of negative feedback loops through the financial markets or the banking system. Growth in 2020 could amount to –4.5 % in this scenario. Next year, economic output would only grow at a very slow pace of 1.0 %.

2. Economic policy measures

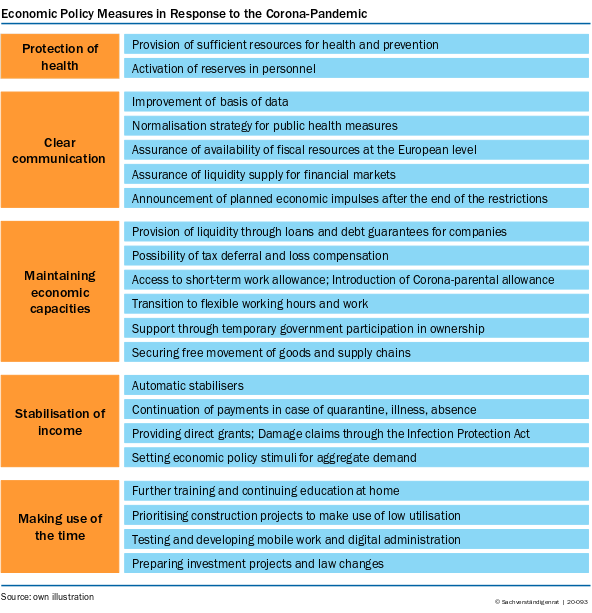

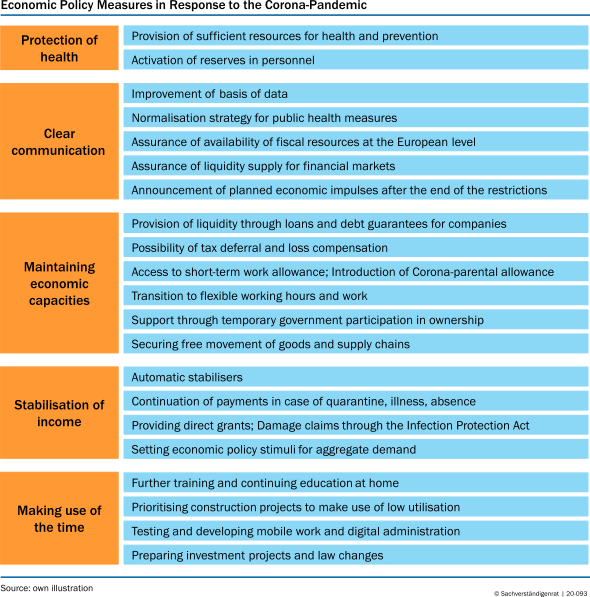

(6) First and foremost, the priority is to enable the health system to provide adequate care to patients and to limit the spread of the virus by implementing suitable measures, particularly measures to reduce the risk of contagion through social contact. The health system must be given sufficient financial resources to do so. At the same time, channels should be used to mobilise personnel reserves and emergency capacities.

(7)Clear communication of essential measures and plans can promote acceptance of public health interventions and help reduce uncertainty in the population and the business sector. This could help limit the economic costs of the crisis. Policy-makers should communicate their criteria and timeline for public health restrictions in a kind of normalisation strategy. Evidence-based decisions and the right timing of measures require a reliable and broad data base. This includes broadening the virus-testing and providing real-time data on economic activities, for example.

If the Member States of the euro area send a clear signal to provide additional fiscal resources immediately, if needed, via existing instruments, such as the European Stability Mechanism (ESM), they will be able to stabilise expectations on the financial markets. The conditions for the use of the instrument could be reduced to the necessary minimum for the subsequent reduction in the debt ratio. The European Central Bank (ECB) has already done its part to stabilise expectations. It has guaranteed a sufficient supply of liquidity and additional asset purchases. A link to the ESM would also enable the ECB in extreme cases to specifically buy bonds of individual Member States even on a large scale within the framework of Outright Monetary Transactions (OMT). Standard demand stimulus measures that aim to boost economic activity in the short term do not hold much promise as long as the various restrictions on social and economic activities continue. Nevertheless, the expectations of households and businesses can be positively influenced by announcing economic policy stimuli for the time after the restrictions at an early stage.

{kind=link}

{kind=link}

{kind=link}

(8) To support economic recovery after the downturn, policy-makers can focus activities in three specific areas. Firstly, economic capacities should be maintained as much as possible beyond the downturn. The Federal Government's broad package of measures that is designed to protect businesses and workers from the impact of the crisis is therefore welcome. It comes at the right time. Liquidity support, tax deferrals and guarantees aim to help businesses avoid having to file for bankruptcy due to the abrupt fall-off in demand or bottlenecks in supply chains for intermediate products. The same applies for measures taken by the ECB to ensure lending by banks. With easier access to short-time working allowance and more flexible working time arrangements, businesses can avoid having to let go workers whom they will likely need again urgently once the epidemic subsides. All actions should ensure that the drop in economic output is contained quickly and effectively and that the "pronounced V" risk scenario does not materialise.

If the recovery takes longer – as depicted in the "long U" risk scenario, for instance – public involvement could also ensure the survival of selected businesses. In this context it is important to ensure that government participation in ownership remains temporary, and that the Federal Government and the Länder have an exit strategy from the outset. Silent participations may be a solution to enable a subsequent exit. During the entire time, the free movement of goods should be maintained to the greatest extent possible and the cross-border movement of persons should resume once the public health measures come to an end.

(9) Secondly, economic policy measures serve to stabilise income. In Germany, this involves well-established institutions that act as automatic stabilisers, such as the tax system, unemployment insurance, the health insurance system, the continued payment of wages in the event of quarantine or illness, and the social partnership between employers and trade unions. The Federal Government has also agreed to provide direct grants for households or self-employed persons particularly hard hit by the crisis.

If the economy develops more along the lines of the "long U" risk scenario, fiscal demand stimuli can increase the income of households and businesses and therefore help bring about a faster recovery. Different temporary and permanent options – with advantages and disadvantages – are available for this, such as a larger investment program, corporate tax cuts, the abolition of the solidarity surcharge, transfers, simplified depreciation rules or an increase in spending on education and research. Not least against the backdrop of this scenario, it is important to bear in mind that fiscal resources are not unlimited and it is therefore vitally important to concentrate on effective measures at the given time.

(10) Thirdly, optimum use should be made of the time during which the public health measures are in place in order to support the recovery and long-term economic development. The period in which people are at home and not in the workplace can be used for further training and continuing education that is important for structural change. Relevant offerings could be supported and incentives provided.

As long as the construction sector remains unaffected by restrictions on production, priority could be given to projects by which faster progress can be made when utilisation is low, such as in the case of schools, the public transport system or roads. The time could also be used to plan investment projects that could be implemented when the restrictions are lifted. Furthermore, the restrictions make fast progress on digitalisation imperative for businesses and public administration.

Your browser is outdated

Please update your Browser to view this website properly.

You will need at least Internet Explorer 11 to see our interactive charts.

Mozilla Firefox or alternatively Google Chrome will provide the best experience for this website. Update your browser now