PRESS RELEASE

Creating new prospects for tomorrow – Not squandering opportunities

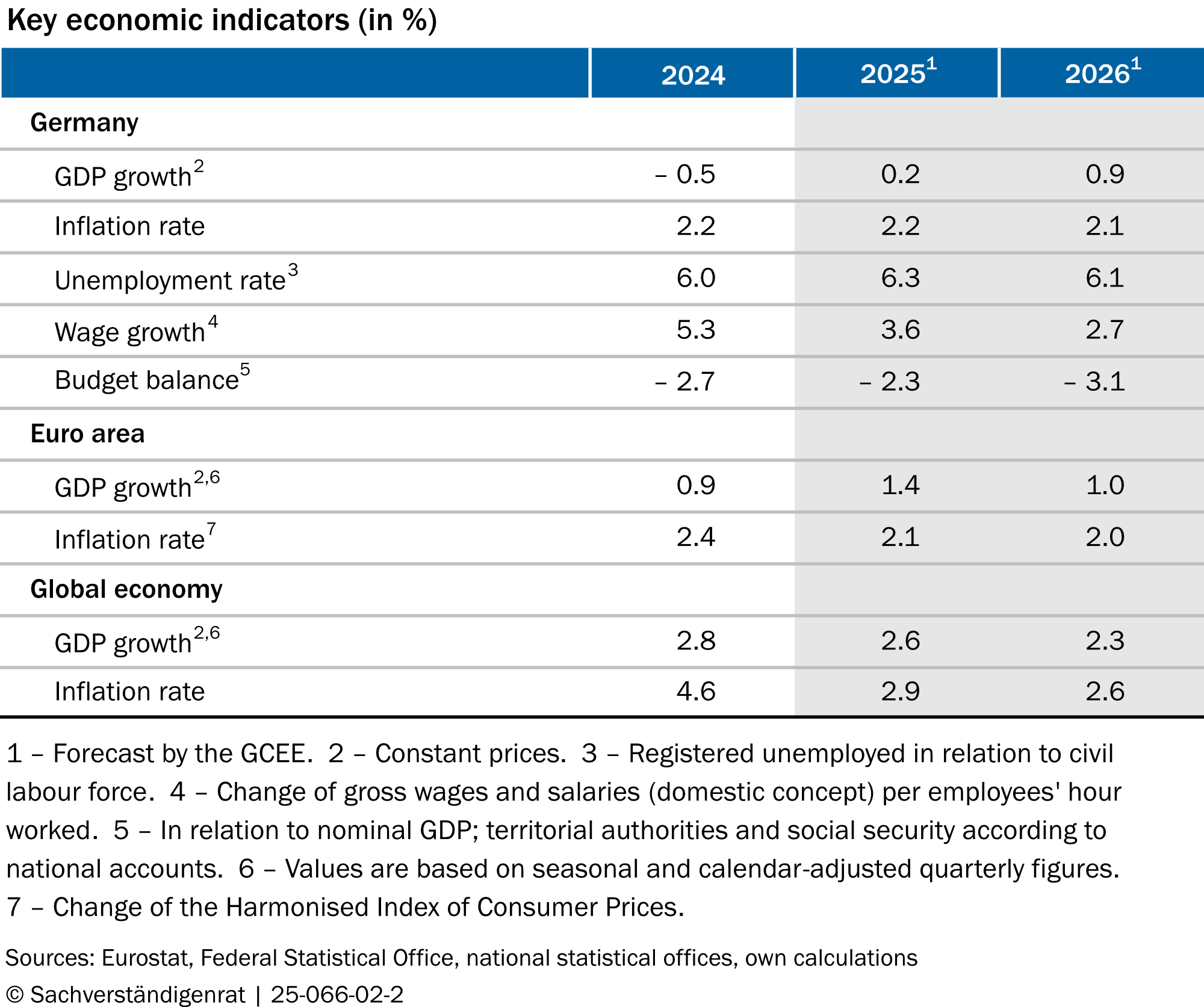

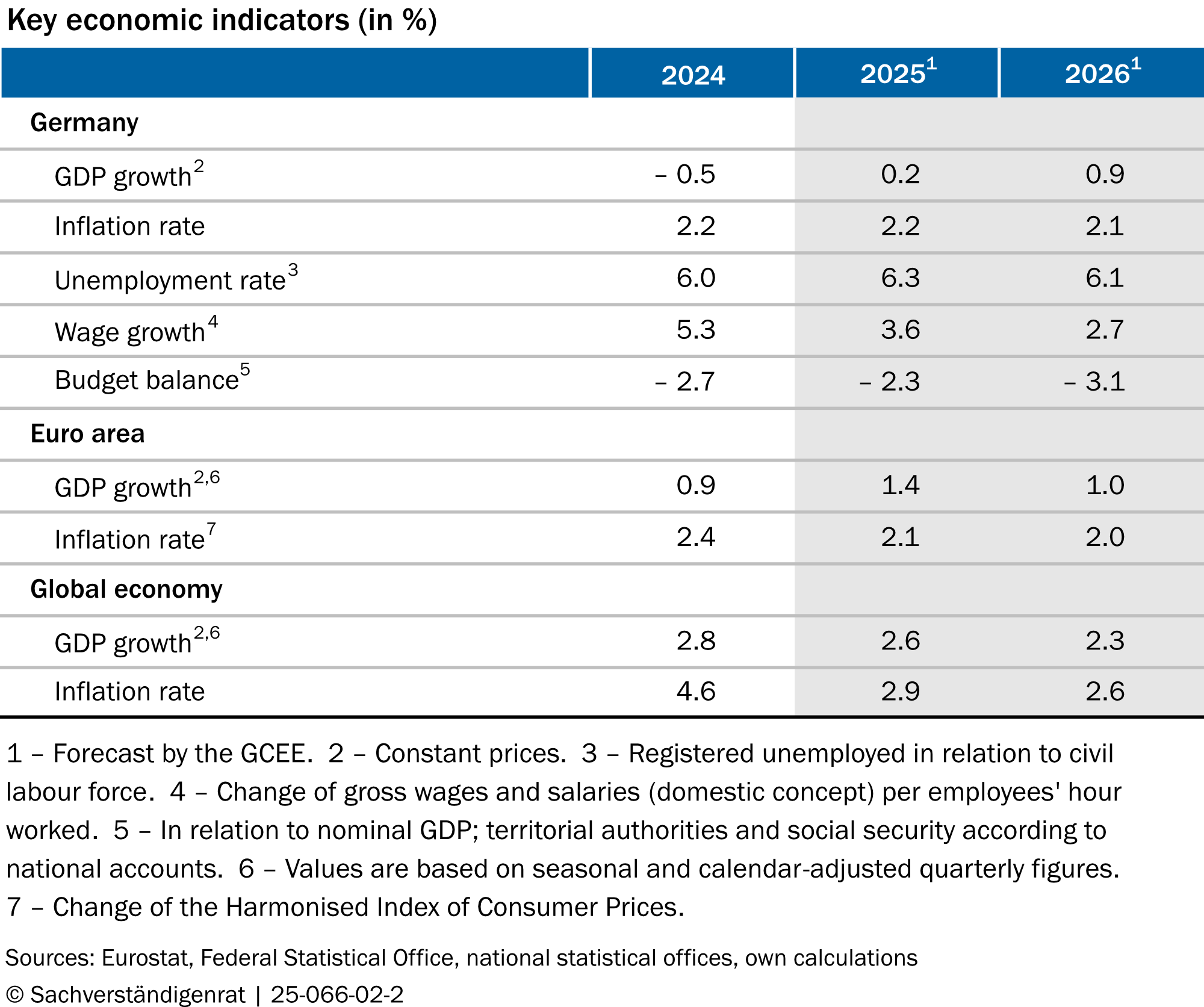

- The German economy continues to experience a period of weakness. Gross domestic product (GDP) is expected to grow by 0.2 % this year and 0.9 % in 2026.

- If the Special Fund was used entirely for additional expenditures and in an investment-oriented way, it would have a significantly stronger impact on economic growth than under the currently planned expenditure path.

- Greater integration of the European single market and capital market could significantly boost GDP. In order to strengthen defence capabilities, Europe should procure defence equipment in a coordinated manner and jointly promote military innovations.

- The recently approved corporate tax cuts promise a moderate increase in GDP and investment. A tax reform that reduces distortions in company investment and financing decisions would be significantly more beneficial in the long term.

- To design a more uniform taxation of all types of assets and align it more closely with the ability-to-pay principle, the inheritance tax should be reformed and the preferential tax treatment for business assets should be reduced significantly. Generous deferral of the tax burden can reduce the liquidity burden on businesses.

After two years of recession, the German economy is currently stagnating. To return to a path of growth, its productivity must increase, in particular through more innovation and investment. “In view of the current challenges, Germany must develop new growth perspectives as well as security policy prospects. The opportunities arising from the Special Fund for Infrastructure and Climate neutrality must not be squandered,” says Monika Schnitzer, chair of the GCEE.

The currently planned expenditure from the Special Fund for Infrastructure and Climate neutrality (SVIK) will have only a small positive effect on gross domestic product (GDP) because, up to now, it is mainly used for budget reallocations and to finance consumptive

expenditure. The effect would be significantly greater if the funds were used entirely for additional expenditure and investment. The recently approved corporate tax cuts will moderately increase investment and GDP growth. However, a more neutral design of corporate taxes could have a significantly greater impact. The European single market for goods and services has enormous potential to turn the EU into an attractive business location. At present, however, the EU is far from realising its full potential. Trade barriers continue to hamper the cross-border movement of goods, services, people and capital. In Germany, private wealth accumulation, especially for retirement, should be strengthened. Inheritances as well as gifts should be taxed more uniformly in order to align taxation more closely with the ability-to-pay principle.

Economy with moderate momentum

The German economy remains weak. While it is likely to grow in 2025 for the first time since 2022, growth will be minimal. The GCEE expects price-adjusted GDP growth of 0.2 per cent compared to the previous year. Weak private investment activity and a weak export economy are weighing on overall economic growth. The GCEE expects GDP to grow by 0.9 per cent in 2026. This is likely to be driven by increased government spending and the high number of working days due to calendar variations.

Anchoring the additionality requirement in the Special Fund

Less than 50 per cent of the expenditures from the SVIK can be classified as additional expenditure for infrastructure and climate neutrality. As a result, the expected growth effects are lower and the increase in the debt-to-GDP ratio is higher than under an investment-oriented expenditure plan. To ensure that the SVIK funds are spent on investments that go beyond pre-existing plans, legal provisions should be designed to guarantee additionality. Moreover, when calculating the investment ratio in the core federal budget, defence expenditure should not be taken into account. Planned but not executed investments should be carried over to the next financial year via a binding catch-up rule. There is also a lack of clear provisions for the SVIK funds going to the federal states and the Climate and Transformation Fund to ensure the additionality of their use. To ensure the sustainability and crisis resilience of public finances, expenditures on infrastructure and defence should be financed from the core budget once again in the future.

Exploiting the potential of the Single market

The EU has fallen short of its economic potential. To take full advantage of the opportunities offered by the European single market, trade barriers must be removed, the capital market strengthened and fragmentation in the defence market overcome. A deeper European single market can contribute significantly to increasing productivity and economic growth. Territorial supply restrictions should be reduced and regulations harmonised, for example by introducing a 28th regime in company law.

Defence capabilities could be significantly strengthened through a joint European approach, provided it is designed efficiently. Pooling demand for defence equipment at the European level would create incentives for firms to scale up production. At the same time, coordinated procurement would strengthen the negotiating position of the EU member states vis-à-vis suppliers and create cost advantages. In addition, military innovation should be promoted through joint research and development projects.

Relieving the burden on companies, making taxation efficient

At 28.5 per cent, the effective tax burden on companies in Germany is high compared to other advanced economies or neighbouring European countries. The recently approved corporate tax cuts promise a moderately positive effect on investment and income – accompanied by a noticeable, but temporary decrease in total tax revenue.

If corporate taxes were designed more neutrally, for example by treating equity and debt financing equally for tax purposes, this would strengthen investment incentives in the long term and reduce the incentive for excessive debt. Suitable reform models include the allowance for corporate equity, which allows for tax deduction of the notional cost of equity, or cash flow taxation with immediate expensing. Although the transition to such neutral taxation is likely to be accompanied by significant fluctuations in revenue during the transition phase, this form of taxation would be worthwhile in the long term, given its large potential.

Strengthen private wealth accumulation, tax inheritances more evenly

Wealth inequality in Germany is high by European standards, but has remained stable since 2010. The wealth accumulation of private households can be strengthened through greater participation in capital markets and improved government programmes for wealth accumulation. The GCEE proposes a new state-subsidised long-term investment account that serves both private retirement provision and general wealth accumulation.

Different types of assets are taxed unevenly in the case of inheritances and gifts. Business assets in particular benefit from preferential tax treatment. The inheritance and gift tax should be reformed to ensure more uniform taxation of all types of assets. To this end, the preferential tax treatment for business assets should be significantly reduced by considerably restricting the exemption rules. Both the inheritance and the gift tax should be aligned more closely to the ability-to-pay principle.

{kind=link}

{kind=link}

{kind=link}

{kind=link}