![[Translate to english:]](/fileadmin/_processed_/4/6/csm_Header_klein_Bild_option4_4b3dd04499.jpg "[Translate to english:]")

Creating new prospects for tomorrow – not squandering opportunities

EXECUTIVE SUMMARY

Click to share

(1) The German economy is stagnating this year, after experiencing a recession in 2023 and 2024 according to the latest data. In addition to cyclical factors, this weakness reflects structural changes and geopolitical shifts that are undermining the traditional German export model. Amid a changing geopolitical order and growing uncertainty about the reliability of US security guarantees for European NATO members, long-standing economic and security frameworks are under increasing pressure to adapt. At the same time, the continued fragmentation of the European Single market for goods, services and capital prevents Europe from an effective response to these new global challenges. Yet, Germany’s current economic weakness is not solely explained by these external factors. Domestic aspects such as a sustained decline in the competitiveness of German industries and the ongoing demographic aging are also contributing factors.

The Federal Government has sought to address the increased security and economic challenges with a fiscal package aimed at strengthening the government’s investment capacity and at funding higher defence expenditures. However, the implementation of these measures needs significant improvements in order to achieve additional and productive investment. Else, growth opportunities risk being squandered and the long-term sustainability of public finances could come under strain.

(2) In its 2025 Spring Report, the GCEE presented an initial assessment of the fiscal package. ITEM 488 FF. The analysis primarily addressed questions regarding its design and macroeconomic implications. In addition, the GCEE examined how a consistent reduction of unnecessary bureaucracy could reduce costs for firms and remove barriers to growth. ITEMS 588 FF. Finally, the Council discussed strategies for managing regional heterogeneity in structural change and its effects. ITEMS 693 FF.

(3) In its 2025/26 GCEE Annual Report, the GCEE builds upon these analyses and considerations. CHART K1 It shows why the fiscal package under its currently planned implementation, in particular the Special Fund for Infrastructure and Climate Neutrality (SVIK), is unlikely to lead to sufficient additional investments. Based on this analysis, the Council proposes adjustments to the allocation and use of funds that would both enhance the overall macroeconomic impact and limit the increase in the debt-to-GDP ratio, which is driven by increased defence spending. ITEM 114

In three further chapters, the GCEE examines additional key areas of economic policy that are essential for overcoming the current crises. There is a need for progress in integrating the European markets for goods, services and capital as well as strengthening European defence capabilities for Germany and the European Union to assert their roles, economically and strategically, in a new multipolar world order. ITEMS 171 FF. In Chapter 4, the GCEE addresses the corporate tax reform initiated by the Federal Government and finds that, while the reform will help to alleviate the tax burden for firms, corporate taxation continues to distort financing and investment decisions due to the unequal tax treatment of equity and debt financing. This distortion is associated with considerable welfare losses in the long term, which could be mitigated by further reform measures. ITEMS 260 FF. In the fifth chapter, the Council reports on the distribution of wealth in Germany, as mandated by its statutory duties, and highlights how to improve wealth accumulation in Germany via stronger incentives for participation in capital markets. Finally, the GCEE emphasises the need to reform inheritance and gift taxation to ensure greater consistency with the principle of equality across all asset types, notably by reducing preferential treatment for business assets. ITEM 351 FF.

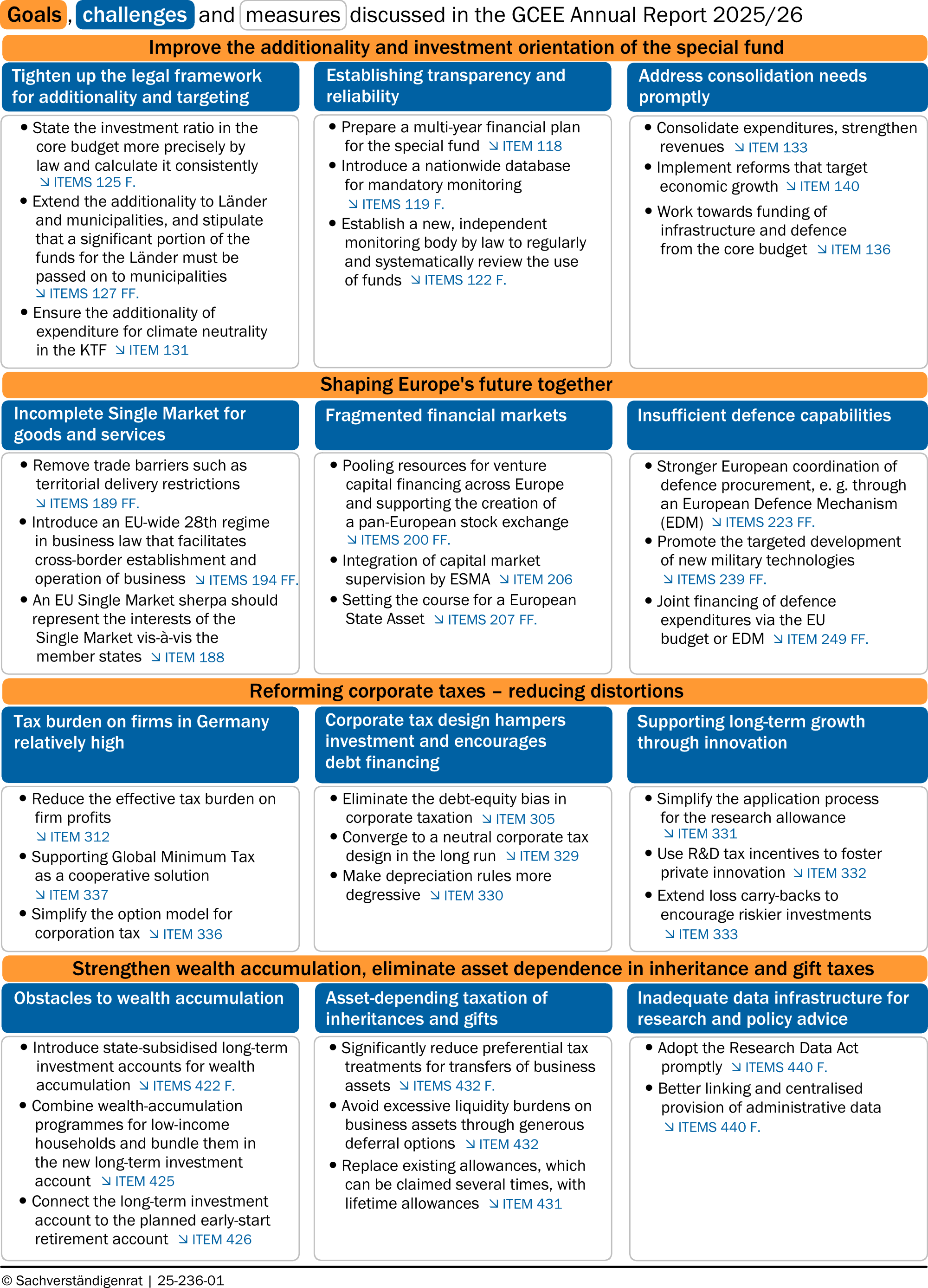

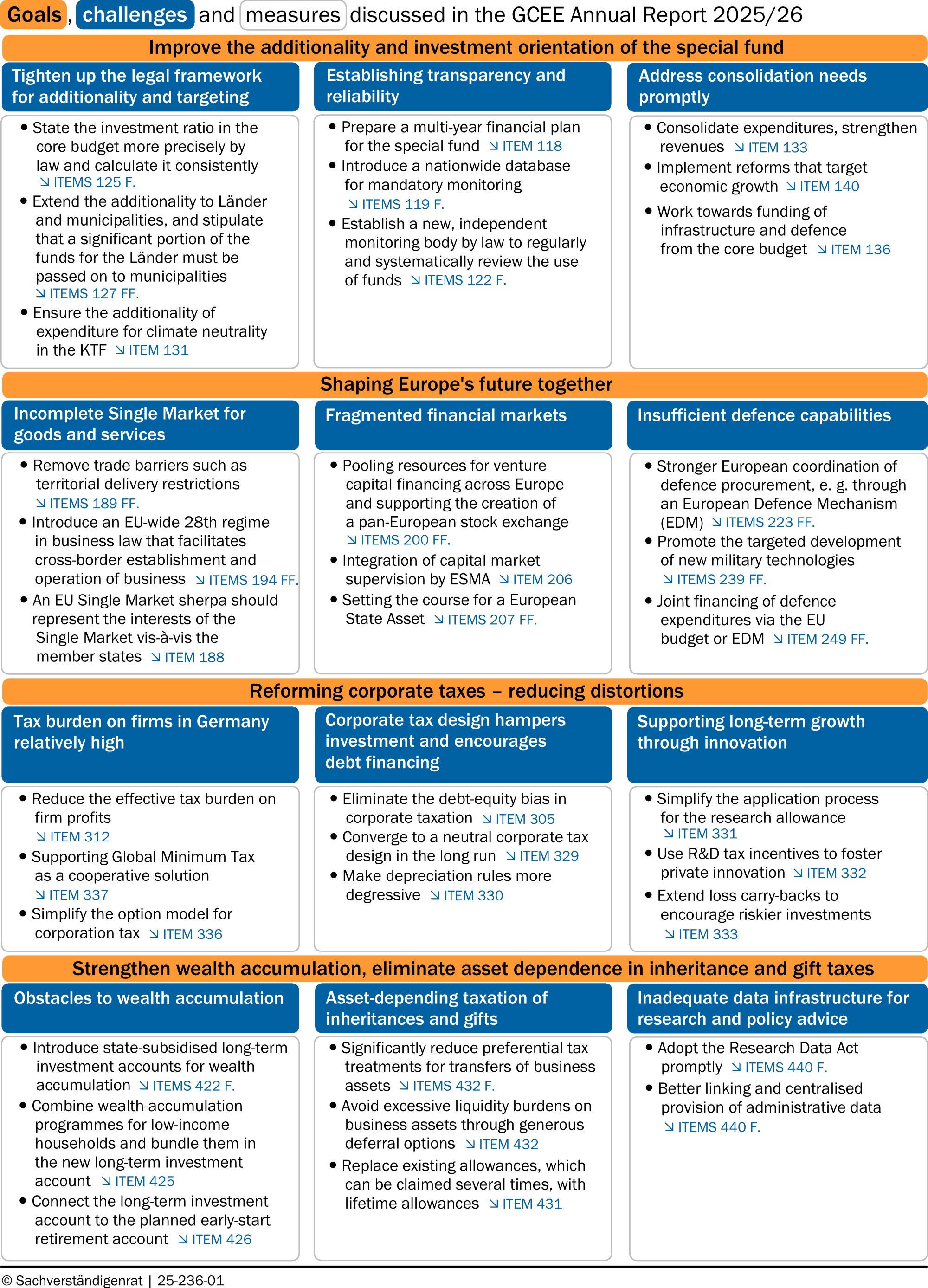

- State the investment ratio in the core budget more precisely by law and calculate it consistently ITEMS 125 F.

- Extend the additionality to Länder and municipalities, and stipulate that a significant portion of the funds for the Länder must be passed on to municipalities ITEMS 127 FF.

- Ensure the additionality of expenditure for climate neutrality in the KTF ITEM 131

- Prepare a multi-year financial plan for the special fund ITEM 118

- Introduce a nationwide database for mandatory monitoring ITEMS 119 F.

- Establish a new, independent monitoring body by law to regularly and systematically review the use of funds ITEMS 122 F.

- Remove trade barriers such as territorial delivery restrictions ITEMS 189 FF.

- Introduce an EU-wide 28th regime in business law that facilitates cross-border establishment and operation of business ITEMS 194 FF.

- An EU Single market sherpa should represent the interests of the Single market vis-à-vis the member states ITEM 188

- Pooling resources for venture capital financing across Europe and supporting the creation of a pan-European stock exchange ITEMS 200 FF.

- Integration of capital market supervision by ESMA ITEM 206

- Setting the course for a European State Asset ITEMS 207 FF.

- Stronger European coordination of defence procurement, e. g. through an European Defence Mechanism (EDM) ITEMS 223 FF.

- Promote the targeted development of new military technologies ITEMS 239 FF.

- Joint financing of defence expenditures via the EU budget or EDM ITEMS 249 FF.

- Reduce the effective tax burden on firm profits ITEM 312

- Supporting Global Minimum Tax as a cooperative solution ITEM 337

- Simplify the option model for corporation tax ITEM 336

- Eliminate the debt-equity bias in corporate taxation ITEM 305

- Converge to a neutral corporate tax design in the long run ITEM 329

- Make depreciation rules more degressive ITEM 330

- Introduce state-subsidised long-term investment accounts for wealth accumulation ITEMS 422 F.

- Combine wealth-accumulation programmes for low-income households and bundle them in the new long-term investment account ITEM 425

- Connect the long-term investment account to the planned early-start retirement account ITEM 426

- Significantly reduce preferential tax treatments for transfers of business assets ITEMS 432 FF.

- Avoid excessive liquidity burdens on business assets through generous deferral options ITEM 432

- Replace existing allowances, which can be claimed several times, with lifetime allowances ITEM 431

- Adopt the Research Data Act promptly ITEMS 440 F.

- Better linking and centralised provision of administrative data ITEMS 440 F.

{kind=link}

{kind=link}

1. Moderate economic momentum

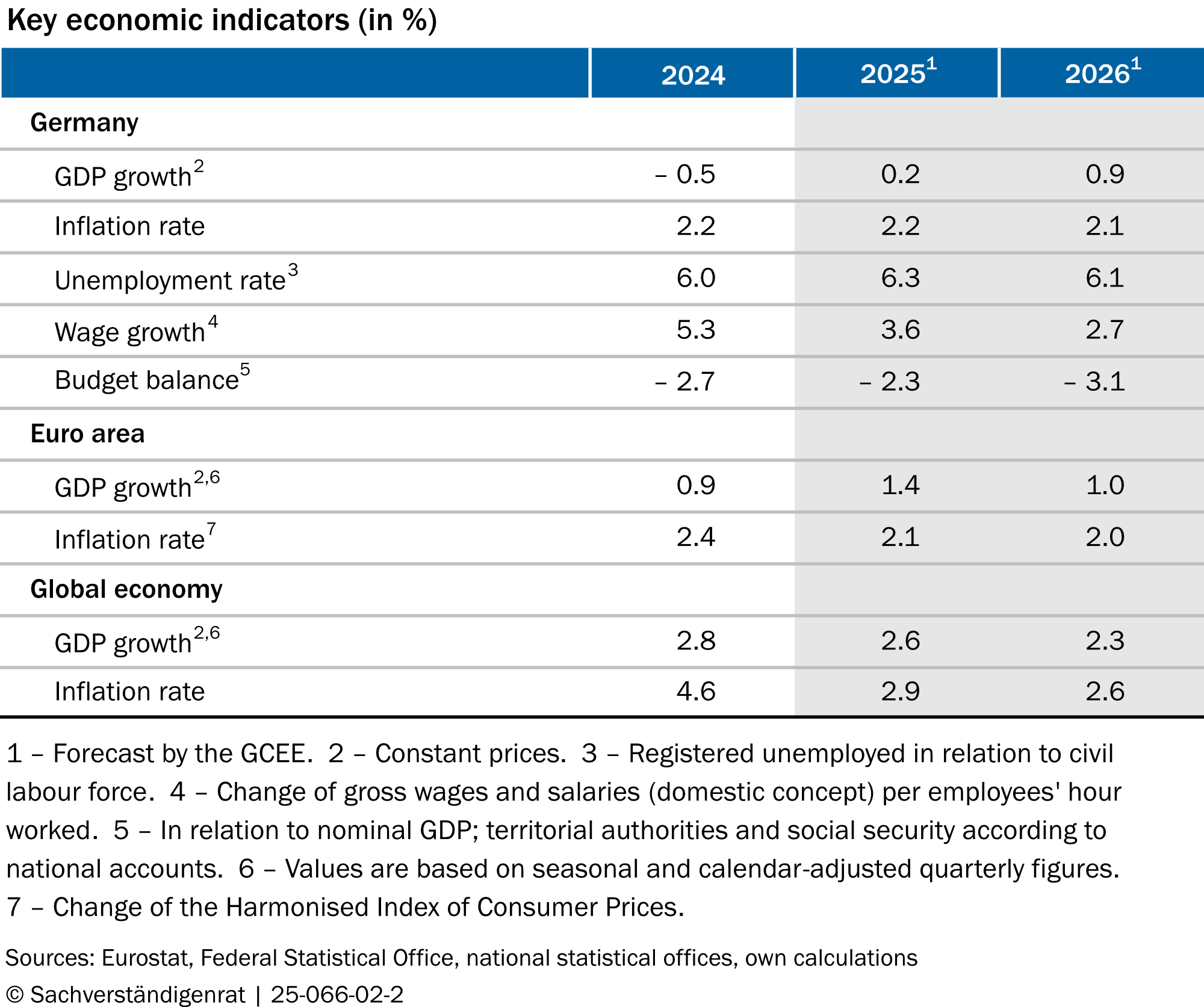

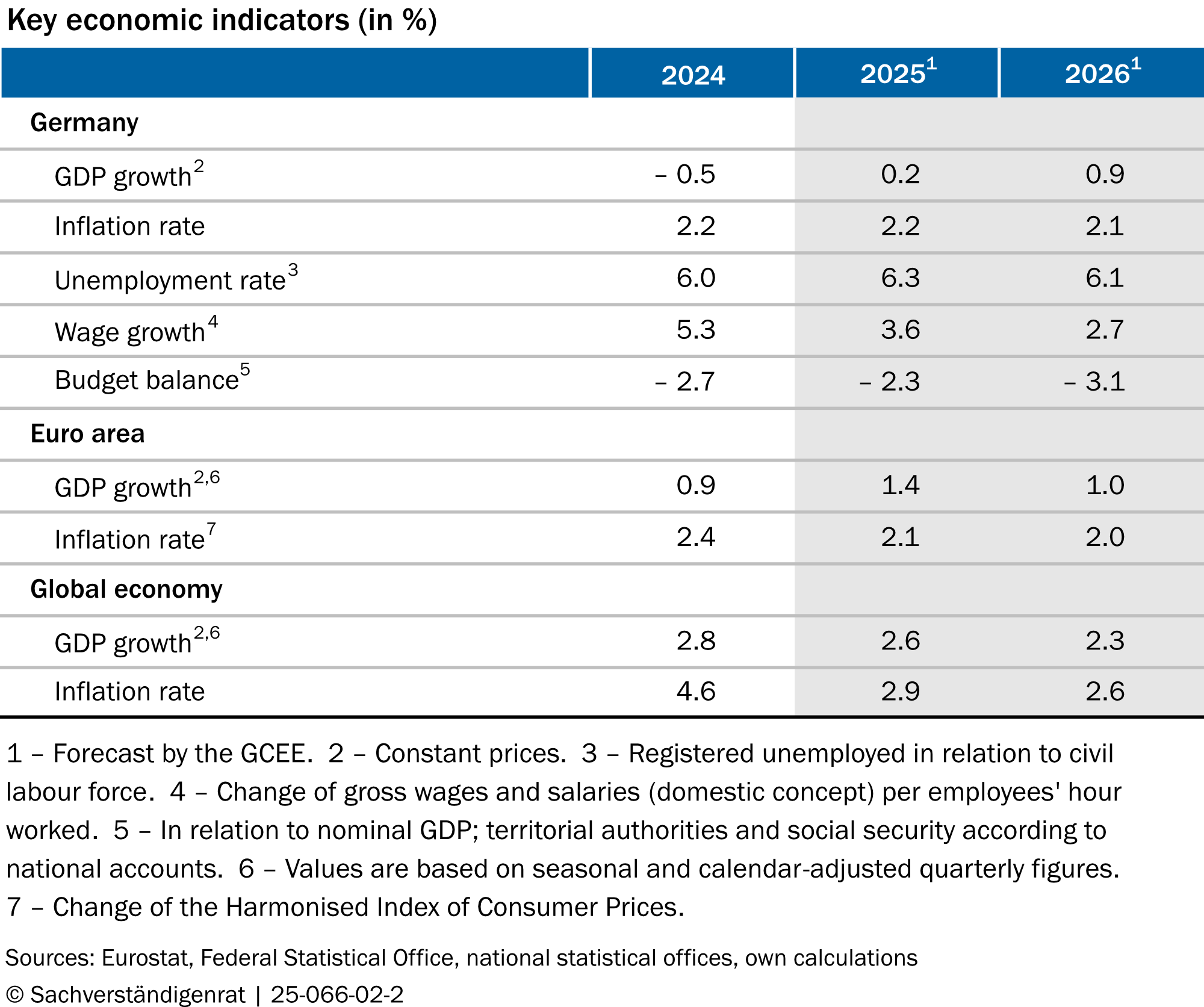

(4) The global economy is currently strongly affected by the protectionist and erratic trade policy of the United States (US). In the first quarter of 2025, this resulted in noticeable front-loading effects in international trade, followed by significant rebound effects in the second quarter. The GCEE expects global gross domestic product (GDP) to grow by 2.6 % and 2.3 % in 2025 and 2026, respectively. However, the German economy is likely to benefit less from global growth than in previous decades, as German firms have become less competitive in international markets (GCEE Annual Report 2024, item 44). China is increasingly emerging as a direct competitor for German industrial producers and is benefiting from lower export prices, which in August 2025 were 17.3 % below their 2022 level. ITEM 14 Over the same period, export prices in the euro area increased by 14.4 %. ITEM 10

(5) The German economy continues to experience weak growth. ITEM 36 The tentative recovery that had begun in the manufacturing sector during the summer of 2025 has since lost momentum. ITEM 46 The volume of orders from abroad increased in the first half of 2025, but reverted back to its beginning-of-year level by August. Business expectations improved in October, but remain subdued. Exports have been declining since 2023 and are expected to continue to dampen economic growth in 2025, while imports are on the rise. ITEM 61 FF. Since the beginning of 2025, German exports exhibit an additional strain resulting from the protectionism and volatility of US trade policy as well as the appreciation of the euro. Private consumption spending rose sharply in the first quarter of 2025, but no further momentum is expected for the forecast period. ITEM 51 F. While the saving ratio normalised in the first half of 2025, consumption growth is projected to remain moderate in 2025 and 2026, given only marginal increases in real wages. The volume of firm investments is likely to remain subdued, reflecting low capacity utilisation and weak sales both domestically and abroad. ITEM 55 FF. However, the fiscal spending from the fiscal package adopted in March 2025 is likely to provide expansionary impulses for construction and gross fixed capital formation in machinery and equipment from next year onwards. ITEM 57

(6) The GCEE expects German GDP to grow by 0.2 % in 2025. This represents a 0.2 percentage point upward revision of its forecast compared with the spring report. ITEM 39 In addition to unexpectedly strong front-loading and rebound effects in the first half of the year, this revision is also due to a revision of the GDP data by the Federal Statistical Office. BOX 4 For 2026, the GCEE expects GDP growth of 0.9 %. CHART K2 Consumer price inflation is expected to average 2.2 % in 2025 and 2.1 % in 2026, while core inflation is expected to be 2.7 % in 2025 and 2.5 % in 2026.

The forecast is subject to downside risks that may arise from the implementation of the Special Fund for Infrastructure and Climate Neutrality. ITEM 80 One risk is that the funds could be disbursed more slowly than assumed, thereby reducing the expected fiscal stimulus in 2026. Another risk is that, depending on capacity utilisation, the fiscal package could exert stronger-than-anticipated price pressure.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

2. Improving the additionality and investment orientation of the special fund

(7) The €500 billion Special Fund for Infrastructure and Climate Neutrality (SVIK) is designed to contribute to three goals until 2037: reducing the backlog in public infrastructure investment, working towards climate neutrality and stimulating economic growth. The growth effects could be substantial, if the special fund was deployed for additional rather than already planned expenditures and for investment rather than consumption purposes. ITEMS 109 FF. AND 527 Positive growth effects are essential also to contain the increase in the debt-to-GDP ratio resulting from the credit financing of the Special Fund and even more so, from the exemption rule that enables massively increased defence spending. GCEE simulations show that, under the current SVIK expenditure trajectory (“current policy scenario“), its macroeconomic effects remain small compared to a trajectory with strong investment orientation, CHART K3 TOP while public debt could rise to over 85 % of GDP by 2035. CHART K3 BOTTOM

(8) There are several factors underlying the weak growth effects of the Special Fund in the current policy scenario. At the federal level, there are two key problems. The Basic Law stipulates that the federal government shall use the SVIK solely for additional investment. The Special Fund should not substitute existing budgetary resources, but rather increase investment above the current level. However, the 2025 federal budget and the draft 2026 federal budget both undermine the principle of additionality, ITEM 91 as large shares of the SVIK funds are used to replace regular budget expenditure. In addition, the federal government's share of the SVIK expenditure is often not well-targeted towards investment. ITEM 98 Moreover, for the €100 billion SVIK shares of the federal states and the Climate and Transformation Fund (KTF), there are no institutional mechanisms at all to ensure the funds are spent for additional investment. ITEM 106 Nor are there mechanisms to ensure targeted spending, as the State and Local Infrastructure Financing Act (LuKIFG) lacks clear rules for spending and prioritization based on macroeconomic impact. ITEMS 100 FF.

(9) The effective spending of SVIK funds should be consistently monitored. ITEMS 117 FF. In particular, the establishment of a multi-year financial plan and a central project register, ITEM 119 in conjunction with a legally mandated and independent monitoring body, ITEMS 122 F. would enhance transparency.

The legal framework for compliance with additionality needs more clarification. The investment quota in the federal government's core budget should be calculated in a transparent and uniform manner that is economically meaningful. The level of additional investment should not merely reflect budget planning but should actually be achieved on average over multiple years. ITEMS 125 F. At the level of the federal states and municipalities, where no explicit additionality requirement currently applies to the use of SVIK funds, at least the non-SVIK spending on public investments should be maintained at their previous levels. ITEMS 127 FF. As municipalities are the main providers of public investment, they should receive at least 60 % of the funds from the Länder on a binding basis.

The SVIK should not be used to create fiscal leeway in the core budget that allows in turn for the funding of measures of questionable economic merit, such as expanding maternity pensions or increasing the income tax allowance for commuters. ITEM 133 Instead, the financing proviso in the coalition agreement should be taken seriously in order to ensure the long-term stability of the federal budget. ITEMS 132 FF. Spending on public infrastructure needs to come from the core budget once the current backlogs have been resolved. ITEM 136 Likewise, for the sustainable public finances require defence spending to come from the core budget, once the existing backlog has been covered and the European exemption has expired. ITEM 137 In the long term, additional fiscal space should be created through reforms that generate growth and broaden the tax base. ITEMS 139 F.

A DIFFERING OPINION ITEMS 141 FF.

3. Securing Europe's future together

(10) The European Union (EU) is the world's second-largest economically integrated area, home to 450 million people and 26 million firms. However, productivity growth in the EU has slowed significantly in recent decades compared to the US. At the same time, Europe’s level of security has fundamentally deteriorated following Russia's attack on Ukraine. This shift in the geopolitical order is increasing pressure on the EU to strengthen its economic and security policy capabilities in order to safeguard its strategic and economic sovereignty.

(11) Despite considerable progress in integration, the EU continues to fall short of unlocking its full economic potential. Considerable barriers to trade persist in the Single market for goods and services, limiting competition and thereby constraining efficiency gains. Model-based analyses indicate that a deeper Single market without these barriers could raise the EU's real GDP significantly more than has been achieved through the integration steps taken to date. CHART K4 TOP Another impediment to economic dynamism is the insufficient integration of European capital markets. Different regulatory frameworks and an incomplete banking union continue to generate inconsistent financing conditions across member states. This fragmentation hampers the efficient allocation of capital, especially in innovative and high-growth sectors.

(12) To foster long-term productivity growth, the European goods, services and capital markets need to be deepened. This requires, firstly, the reduction of territorial supply restrictions that impede cross-border trade in goods, ITEMS 189 FF. as well as harmonising regulations, for example by introducing a "28th regime" in corporate law. Such a framework would establish uniform cross-border regulations and thus reduce regulatory complexity. ITEMS 194 FF. Furthermore, a reform of capital market supervision is needed in order to overcome supervisory fragmentation and improve the efficiency of capital allocation. ITEMS 206 FF. Improving venture capital access for start-ups would further contribute to narrowing the innovation gap between the EU and the US. ITEMS 200 FF. Finally, the introduction of a "European Safe Asset" could serve as a reliable store of value and serve as collateral and price benchmark for financial transactions, thereby making the euro more attractive as a reserve currency. ITEMS 207 FF. The creation of ESBies (European Safe Bonds), in which member states' government bonds are pooled according to a fixed formula and divided into safe and risky tranches, would be suitable for this purpose. However, given the high debt burden of some EU member states, a new mechanism in case of potential defaults needs to be established. ITEMS 216 FF.

(13) To address the deteriorating security situation of the EU, European defence capabilities need to be strengthened. Although many EU member states have already increased their defence spending in recent years, CHART K4 BOTTOM military equipment remains insufficient. The fragmentation of the EU defence market has made it difficult to meet the EU's needs quickly and comprehensively. BOX 11 member states have continued to favour national suppliers, generating inefficiencies and excess costs in defence procurement. Greater use of EU-wide tendering procedures could promote competition. ITEM 224 In addition, a European procurement agency could strengthen the collective bargaining position of the EU member states vis-à-vis the defence industry by pooling demand. ITEMS 229 FF. Defence planning should be forward-looking and strategic, prioritising innovation and investment in research and development (R&D). ITEMS 239 FF. Any joint financing of European defence capabilities, if carried out via EU bonds, should be designed such that it does not jeopardise the sustainability of European public finances. ITEMS 246 FF.

4. Reducing the tax burden on firms, improving tax efficiency

(14) Taxes on corporate profits – in Germany via the corporate income tax and local business tax – are an important determinant of a country's attractiveness as a location for business and investment. At the same time, these taxes contribute significantly to total tax revenue, accounting for around 12 % in 2024. Germany’s effective average tax burden on corporate profits, currently at 28.5 %, remains high compared to other major advanced economies or neighbouring European countries. CHART K5 TOP This rate is set to decrease below 25 % by 2032 as a result of the recently adopted tax relief programme. ITEM 274 The high tax burden poses particular challenges because, in conjunction with the usual design of the tax system (e.g., the differential treatment of debt and equity funding, the deferred depreciation of investment costs, incomplete loss carry-back), it distorts key decisions of firms (e.g. investment, financing). ITEMS 280 FF. This leads, for example, to inefficiently low investment or high levels of debt.

(15) In light of the current economic weakness, a short-term challenge for corporate taxation is to strengthen private investment activity, ITEMS 280 FF. even though the fiscal space for tax cuts is limited. In the medium to long term, tax policy should focus on reducing tax distortions such as debt-equity bias and move toward a more neutral design of corporate taxation. ITEM 329 F. Further challenges arise at the international level, particularly from the profit shifting of multinational firms, which has intensified as a result of globalisation and digitalisation. ITEM 299 F. Multilateral agreements that had already been reached, such as the global minimum tax, were recently called into question by the withdrawal of the US. ITEM 337 F.

(16) Economic policy can use various tools to adjust the level and design of corporate taxation. Cutting statutory tax rates can provide broad relief for firms, while a - permanent or temporary - expansion of accelerated depreciation options can stimulate investment activity. A conceptual redesign of taxes, e.g., an allowance for corporate equity (ACE)ITEMS 304 F. for nominal capital or a cash flow tax with immediate expensing, ITEMS 307 F. can neutralize distorted incentives in financing and, to a large extent, in investment. Simulations based on a quantitative macroeconomic model show that the tax relief programme promises positive but moderate stimulus for investment and income, with a temporary noticeable decline in total tax revenue. ITEM 317 FF.

The increases in investment and aggregate income that could be achieved in Germany through a more neutral corporate tax design are likely to be significantly larger, ITEMS 323 FF. accompanied, though, by strong fluctuations in tax revenue during the transition phase. CHART K5 BOTTOM One way to mitigate short-term revenue shortfalls is, for example, in the case of an allowance for corporate equity, to limit the tax deduction to the cost of newly accumulated equity capital. Finally, R&D tax incentives are an effective tool that provides technology-neutral incentives for firms to innovate. ITEM 297 F. This promises lasting growth effects. Germany has already taken a significant step in this direction with its research allowance, which should be further simplified.

5. Strengthen wealth accumulation, tax inheritances and gifts more evenly

(17) Relative wealth inequality in Germany is high compared to other European countries. It has increased since reunification, but has remained relatively constant since the 2010s. ITEM 352 Pension entitlements are not included in these comparisons due to their non-tradable nature. Their inclusion would lead to a lower level of wealth inequality. ITEM 357 Households at the lower end of the income distribution accumulate less wealth, primarily because their low incomes limit their ability to save, CHART K6 TOP but also because their savings tend to yield lower returns. Wealth mobility over the life cycle is lower at the upper and lower ends of the distribution in Germany than in the middle. ITEMS 363 FF. International studies reveal a high correlation of wealth between parents and their children, which is particularly influenced by inheritances and gifts. ITEMS 372 FF. For Germany, the estimated share of wealth attributable to inheritances and gifts is 30 % to 50 %.

(18) Government programmes designed to foster wealth accumulation fail to adequately reach households at the lower end of the wealth distribution. ITEMS 397 F. At the upper end of the wealth distribution, the uneven taxation of inheritances and gifts depending on the type of asset can impede intergenerational wealth mobility. ITEM 414 CHART K6 BOTTOM The biggest distortion comes from the preferential tax treatment of business assets. ITEMS 383 FF. Such preferential rules may also distort decisions on legal form and financing and encourage tax evasion arrangements. ITEMS 416 F.

(19) To strengthen wealth accumulation, the GCEE proposes the introduction of a state-subsidised long-term investment account, designed to strengthen financial security mainly in old age. ITEMS 422 ff. It would target diversified high-yield investments and include a simple, standardised default product, with flexible payout options. Automatic enrolment of all people in the labour force would increase participation, in particular among low-income households. Existing public programmes for wealth accumulation are fragmented and should be simplified into the proposed long-term investment account to strengthen the savings capacity of low-income households. The long-term investment account should be linked to the planned early-start retirement account for children and youths, introducing future generations to the capital market at an early stage.

(20) A reform of inheritance and gift tax should ensure more uniform taxation of all types of assets and thus align taxation more closely with actual abilities to pay. Reforms are needed, in particular, regarding the taxation of business assets and the structure of personal allowances. Under the current system, allowances can be claimed several times. Instead, a lifetime allowance could be introduced for all asset transfers received over the course of one’s lifetime. ITEM 431 The extensive tax relief for business assets below €26 million under the exemption discount should be substantially reduced. ITEM 432 The possibility of a retrospective tax waiver through the exemption test for business assets above €26 million should be abolished or significantly restricted. ITEMS 433 FF. Excessive liquidity burdens at the time of the transfer could instead be mitigated through generous tax deferral arrangements and, if necessary, through reduced tax rates. ITEMS 432 and 437

A DIFFERING OPINION ITEMS 442 FF.

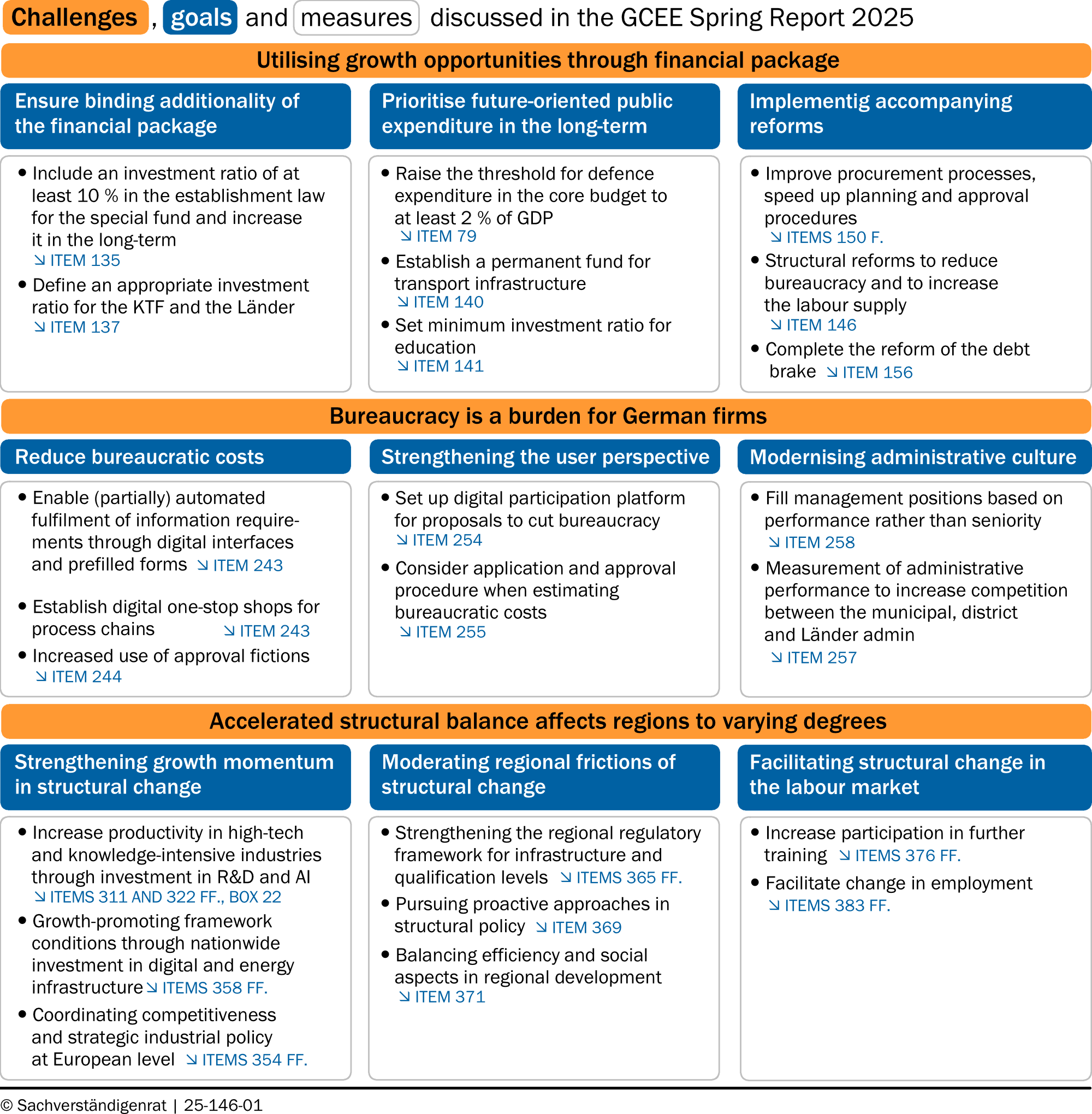

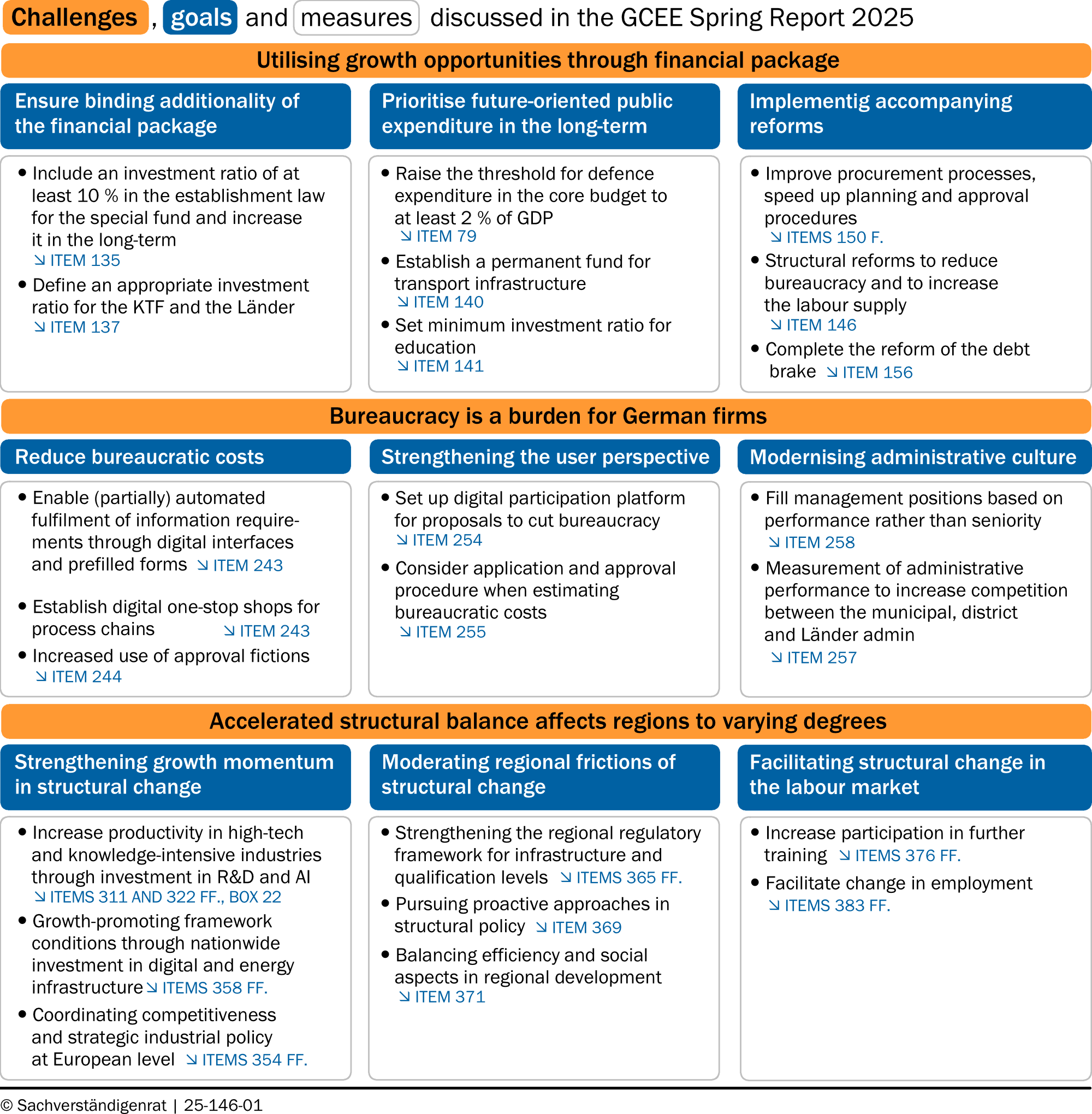

6. Making the most of the fiscal package

Also published in the Spring Report 2025 (21 May 2025)(21) The constitutional amendment, adopted in March 2025, significantly expands fiscal space by introducing an exception to the debt brake for defence spending, establishing a special fund for infrastructure and allowing the federal states to regularly take on limited amounts of structural debt. If used wisely, these measures provide opportunities to modernise the capital stock and revive economic growth. However, the financial package will increase public debt per GDP, especially if the funds are used for government consumption. By contrast, if the funds are used for public investment, CHART K7 the resulting growth may curb the rise in the public debt-to-GDP ratio. ITEMS 532 F.

(22) A key challenge in implementing the fiscal package is therefore to ensure that the funds are used in a way that delivers lasting economic growth. To achieve this, binding rules must be put in place to guarantee that the funds go towards additional investment and not simply replace spending already planned in the core budget. The measures taken so far are not sufficient. They leave considerable room for shifting already planned expenditures from the core budget and financing them through borrowing instead—up to 1.2 % of GDP. ITEM 546 To prevent this, at the very least, the core budget investment quota mentioned in the resolution passed alongside the constitutional amendment should be included in the law establishing the special fund, and this quota should gradually increase. ITEM 548 The same principle of an appropriate investment quota should be applied to funds allocated to the special fund to the Climate and Transformation Fund (KTF) and to the federal states.

(23) At the same time, the long-term financing of investment spending from the core budget should be strengthened. For example, in the area of defence, setting a target of at least 2 % of GDP to be financed directly from the core budget would be appropriate. ITEM 551 To ensure that public investment expenditure in transport infrastructure and education remains a priority even after the special fund expires, a permanent public infrastructure fundITEM 553 with dedicated revenues should be established, along with minimum investment quotas for education. ITEM 554

Whether the fiscal package is compatible with EU fiscal rules is highly uncertain. In any case, compatibility can only be achieved with a strong investment focus and supporting structural reforms. A reform of the debt brake ITEM 569 would still be advisable following the constitutional amendments, in particular to enable more flexible responses to crises.

A DIFFERING OPINION ITEMS 573 FF.

7. Comprehensive reduction of excessive bureaucracy

Also published in the Spring Report 2025 (21 May 2025)(24) German firms are subject to public information and approval requirements, which are often referred to as "bureaucracy". ITEM 588 Excessive bureaucracy hinders economic growth by generating unnecessary costs and distorting firms' decisions on market entry and investment. ITEMS 595 FF. Business surveys show that dissatisfaction with bureaucratic requirements in Germany has increased in recent years. CHART K8 The direct costs of meeting federal information requirements alone amount to around 65 billion euros per year and tie up at least 1.7 % of the total number of hours worked in Germany. Additional costs arise from requirements imposed by the European Union, the federal states and local authorities. There are currently no comprehensive estimates of the indirect costs resulting from distorted firm decisions.

(25) Bureaucratic costs can be higher than necessary for several reasons. ITEMS 619 FF. One reason is that when new laws are drafted, too little attention is sometimes given to how user-friendly or digitisable the associated procedures will be. ITEMS 638 FF. The enforcement of laws can also lead to unnecessary bureaucratic costs for firms, for example due to lengthy approval procedures or fragmented administration involving multiple authorities. ITEMS 633 FF. In the past, some measures have already been taken to reduce bureaucratic costs. ITEMS 643 FF. These include ex-ante instruments such as the „digital check“ ITEM 645 as well as ex-post instruments such as the Bureaucracy Relief Acts. ITEM 647

(26) Despite various selective efforts to reduce bureaucratic costs, there has so far been no noticeable progress. Comprehensive reforms are needed to reduce existing bureaucracy and prevent new legal regulations from creating additional inefficiencies. ITEMS 652 FF. Digitising administrative processes and partially automating information requirements can help to achieve this. Fragmented procedures could be streamlined through one-stop shops, and redundant requirements could be replaced by centralised data retrieval based on the once-only principle. ITEM 656 Approval procedures could be sped up by making greater use of deemed approvals. ITEM 657 To prevent further increases in bureaucratic costs, the legislative process should place greater emphasis on the quality of new regulations, focusing on effectiveness, user-friendliness, and enforceability. ITEM 664 Law enforcement could also be made more efficient by means of better measurement and greater transparency of administrative services. ITEM 670 To implement these measures in a coordinated manner and as quickly as possible, bureaucracy reduction should be made a top priority at the highest level of political decision-making.

A DIFFERING OPINION ITEMS 672 FF.

8. Shaping structural change

Also published in the Spring Report 2025 (21 May 2025)(27) Geopolitical shifts in international trade, rising energy costs due to the Russian war on Ukraine and long-term trends such as decarbonisation, digitisation and demographic aging are all accelerating structural change in Germany. ITEMS 728 FF. So far, the share in value added of the manufacturing sector has been stable over time due to path dependencies and comparative advantages. However, structural change is slowing down overall economic productivity growth, as sectors with relatively low productivity growth, especially services, are becoming increasingly important. This trend is likely to continue. ITEMS 702 FF. Structural change is also accompanied by a shift in labour demand. This can lead to significant frictions and adjustment costs for companies and employees, especially if it occurs very quickly. ITEMS 697 F. While the (relative) importance of occupations in manufacturing is declining, the demand for service occupations and highly qualified labour continues to grow.

(28) Some regions and occupations benefit from structural change, while others are negatively affected. CHART K9 TOP Regions that have already been affected by structural change in the past are likely to face further challenges from today’s key drivers of structural change. Even regions that have so far remained structurally stable and economically strong will also be increasingly affected in the future. CHART K9 BOTTOM These regions are often characterised by high employment shares in knowledge-intensive manufacturing. ITEM 757

(29) Industrial, labour market, regional and structural policies can help reduce the adjustment costs of structural change and improve long-term growth prospects, provided they avoid preserving out-dated economic structures. Further measures are needed to counteract negative effects on growth. ITEMS 762 FF. Investment into digital and energy infrastructure supports productivity-enhancing structural change. ITEMS 771 FF. At the same time, it is important to address social aspects and regional disparities to prevent entire regions from falling behind the overall economic trajectory. ITEMS 776 FF. Social acceptance of structural change depends not only on whether it is possible to improve overall economic performance, but also on providing long-term prospects for disadvantaged regions. In particular, supporting investment and innovation of firms as well as investing into local infrastructure and funding innovation can be used to support economically weaker regions. ITEMS 783 FF.

Instead of using costly and inefficient subsidies to preserve jobs that are no longer competitive, structural change should be accompanied by targeted labor market policies focused on training, upskilling, and retraining. This may ensure that workers are efficiently reallocated to sectors with better long-term prospects. Barriers to upskilling can be removed through attractive qualification measures, a clear and comprehensive system of career counselling, directly reaching individuals at their workplaces, or the subsidisation of training costs. ITEMS 789 FF. Regional labour market hubs can facilitate employment changes to sectors of the economy that benefit from structural change. ITEM 796

A DIFFERING OPINION ITEMS 798 FF.

- Include an investment ratio of at least 10 % in the establishment law for the special fund and increase it in the long-term ITEM 548

- Define an appropriate investment ratio for the KTF and the Länder ITEM 550

- Raise the threshold for defence expenditure in the core budget to at least 2 % of GDP ITEM 492

- Establish a permanent fund for transport infrastructure ITEM 553

- Set minimum investment ratio for education ITEM 554

- Improve procurement processes, speed up planning and approval procedures ITEMS 563 F.

- Structural reforms to reduce bureaucracy and to increase the labour supply ITEM 559

- Complete the reform of the debt brake ITEM 569

- Enable (partially) automated fulfilment of information requirements through digital interfaces and prefilled forms ITEM 656

- Establish digital one-stop shops for process chains ITEM 656

- Increased use of approval fictions ITEM 657

- Set up digital participation platform for proposals to cut bureaucracy ITEM 667

- Consider application and approval procedure when estimating bureaucratic costs ITEM 668

- Fill management positions based on performance rather than seniority ITEM 671

- Measurement of administrative performance to increase competition between the municipal, district and Länder administration ITEM 670

- Increase productivity in high-tech and knowledge-intensive industries through investment in R&D and AI ITEMS 724, and 735 FF., Box 46

- Growth-promoting framework conditions through nationwide investment in digital and energy infrastructure ITEMS 771 FF.

- Coordinating competitiveness and strategic industrial policy at European level ITEMS 767 FF.

- Strengthening the regional regulatory framework for infrastructure and qualification levels ITEMS 778 FF.

- Pursuing proactive approaches in structural policy ITEM 782

- Balancing efficiency and social aspects in regional development ITEM 784

- Increase participation in further training ITEMS 789 FF.

- Facilitate change in employment ITEMS 796 FF.

{kind=link}

{kind=link}

MODERATE ECONOMIC MOMENTUM

- The German economy is in a pronounced phase of weakness. The rising volume of public investment spending is likely to have positive effects during the forecast period, while declining net exports are likely to dampen growth.

- The global economy is slowly adapting to the protectionist and erratic US trade policy. Global economic growth will be subdued in the forecast period.

- The GCEE expects Germany's real GDP to grow by 0.2 % in 2025 and 0.9 % in 2026. Consumer price inflation is expected to rise by an annual average of 2.2 % and 2.1 %, respectively.

IMPROVING THE ADDITIONALITY AND INVESTMENT ORIENTATION OF THE SPECIAL FUND

- The Special Fund for Infrastructure and Climate Neutrality (SVIK) is designed to enable additional investment in infrastructure and for the achievement of climate neutrality. However, the additionality and investment orientation are low in the current financial planning.

- The planned expenditure in the SVIK and on defence will have only a minor impact on growth, meaning that the debt ratio is likely to rise above 85 % of GDP by 2035.

- The SVIK should not be used to create scope for financing questionable measures in the core budget. To ensure this, effective rules on transparency, additionality and targeting are needed.

SECURING EUROPE'S FUTURE TOGETHER

- The European Union is facing considerable challenges, among them weak productivity growth compared to the US, and increasing geopolitical tensions.

- Trade barriers and a different regulatory framework prevent the EU from reaching its economic potential. Reducing territorial supply restrictions can improve the integration of the European single market.

- Joint procurement of defence equipment and promotion of military innovation can significantly strengthen European defence capabilities.

REFORMING CORPORATE TAXES, REDUCING INVESTMENT AND FINANCIAL DISTORTIONS

- The recently approved corporate tax cut in Germany promises a moderate increase in GDP and investment.

- A more fundamental tax reform that reduces distortions in investment and in the financing choices of firms promises instead a strong long-term increase in investment, income and welfare.

- R&D tax incentives should be simplified. They are effective in stimulating private innovation, thereby contributing to productivity growth.

STRENGTHENING WEALTH ACCUMULATION, TAXING INHERITANCES AND GIFTS MORE EVENLY

- Wealth inequality in Germany is high compared to other European countries. The available data does not take pension entitlements into account.

- To strengthen wealth accumulation, the GCEE proposes the introduction of a state-subsidised long-term investment account.

- The current inheritance and gift tax taxes different asset types unevenly. A reform should reduce the preferential tax treatment for business assets and thus align taxation more closely with the ability-to-pay principle.

HARNESSING THE OPPORTUNITIES OF THE FISCAL PACKAGE

- The more investment-oriented and the less consumption-driven the spending, the greater the long-term impact of the fiscal package on gross domestic product (GDP) investment.

- The current regulations permit defence and investment expenditure amounting to 1.2 % of GDP to be shifted from the core budget and financed through borrowing instead. Additional institutional safeguards are needed to ensure that the financial package is genuinely used for additional spending.

- The compatibility of the financial package with the EU fiscal rules is highly uncertain. It can only be ensured through a strong focus on investment spending and accompanying structural reforms.

CUTTING BUREAUCRATIC COSTS: A LEGISLATIVE AND ADMINISTRATIVE OVERHAUL

- Dissatisfaction with bureaucratic requirements has recently increased in Germany. Previous solutions have not brought any noticeable improvements.

- Complex information requirements, inefficient administration and lengthy approval procedures imply that the bureaucratic costs borne by companies are higher than necessary.

- The automation of information requirements and the acceleration of administrative procedures through the use of digital technology and artificial intelligence could cut bureaucratic costs. Consideration of administrative enforcement already during the legislation process could result in more practical regulation.

STRUCTURAL CHANGE IN GERMANY: PRODUCTIVITY, REGIONAL ASPECTS AND THE LABOUR MARKET

- Changes in international trade relations, decarbonisation, digitalisation, artificial intelligence (AI) and demographic change are accelerating structural change.

- In the future, also regions that have so far been successful with stable industry compositions will be affected by structural change, especially if they specialise in knowledge-intensive manufacturing.

- More efficient use of information and communication technologies (ICT) and AI can boost productivity. Attractive training measures and regional funding can improve future prospects, facilitate adaptation and thus also improve the societal acceptance of structural change.

Your browser is outdated

Please update your Browser to view this website properly.

You will need at least Internet Explorer 11 to see our interactive charts.

Mozilla Firefox

or alternatively Google Chrome

will provide the best experience for this website.

Update your browser now