![[Translate to english:]](/fileadmin/_processed_/4/6/csm_Header_klein_Bild_option4_4b3dd04499.jpg "[Translate to english:]")

EXECUTIVE SUMMARY

Click to share

(1) In spring 2026, after a prolonged period of weak growth since 2019, the German economy is facing increased pressure to adapt as a result of recent geopolitical developments. ITEMS 10 AND 13 The Iran war and the resulting sharp rise in crude oil and gas prices, as well as US trade policy, are weighing on economic activity. For Germany, the deterioration in the terms of trade associated with high energy prices entails a loss of purchasing power. ITEM 60 The weakness of the German economy, which has persisted for seven years, is not only cyclical in nature but also has structural causes. These include, alongside the declining competitiveness of German industrial goods on global markets, demographic developments.

(2) Demographic change will not only reduce the potential labour volume over the longer term, but also lead to a substantial increase in social insurance contributions, particularly for pension, health and long-term care insurance. CHART K3 TOP Contribution-based revenue is growing more slowly than expenditure in these social insurance systems. The rise in social insurance contribution rates also affects macroeconomic developments. Higher contribution rates reduce households’ net income and dampen consumption and incentives to work. ITEMS 140 FF. At the same time, they raise labour costs for firms, thereby weighing on employment and investment. Cost pressures are already pronounced in health and long-term care insurance. ITEMS 193 FF. AND 304 FF.

(3) In its 2023 Annual Report, the German Council of Economic Experts discussed reform options for the statutory pension insurance scheme. In its 2026 Spring Report, the Council focuses primarily on health and long-term care insurance. The focus is therefore not only on the short-term outlook for output growth and inflation, but also on the extent to which the expected rise in the social insurance contribution rate to almost 50 % by 2040, assuming current legislation remains unchanged, will impair macroeconomic developments, and how this impact can be mitigated. CHART K1

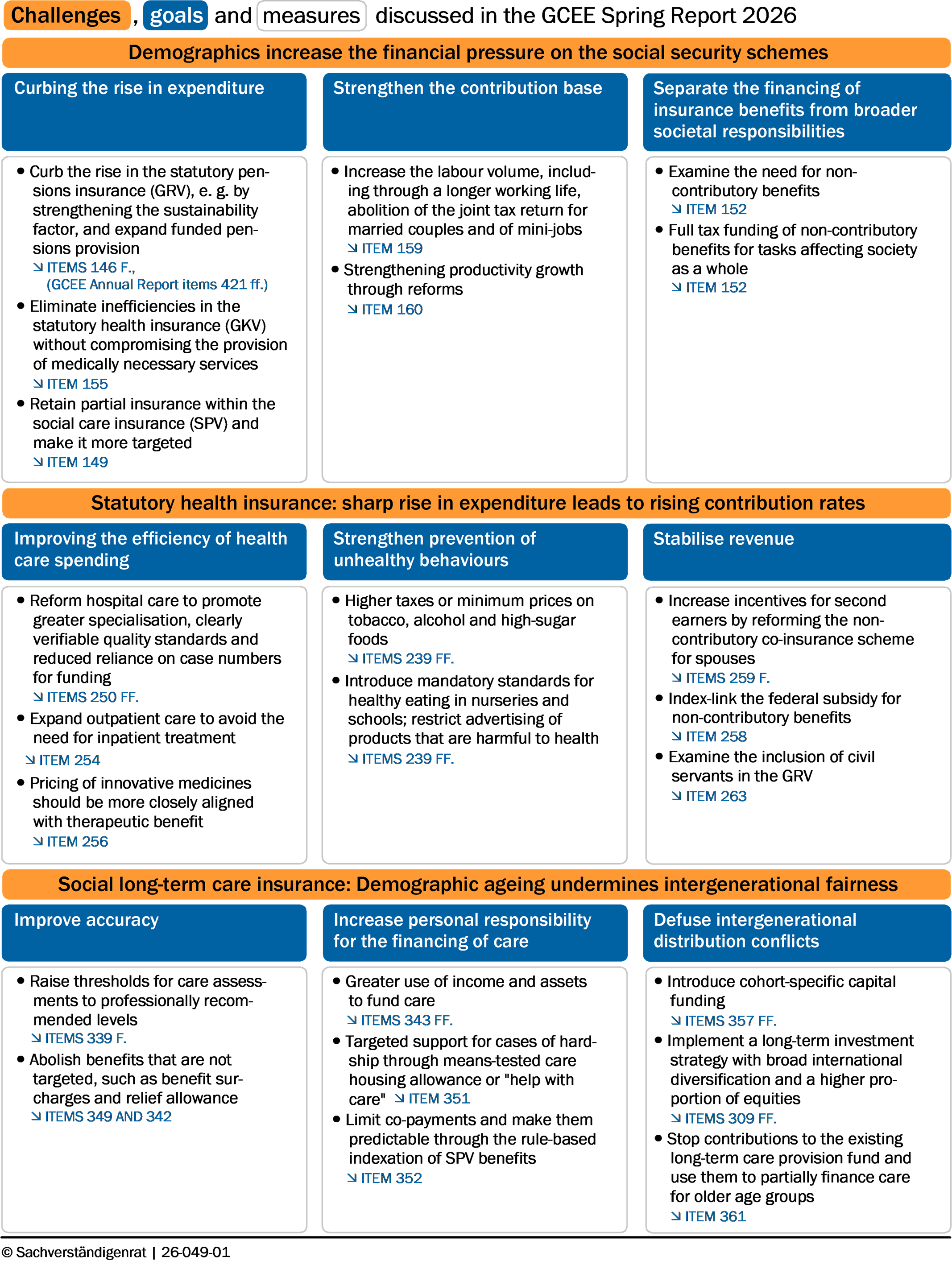

- Curb the rise in the statutory pensions insurance (GRV), e. g. by strengthening the sustainability factor, and expand funded pensions provision Items 146 F.,(GCEE Annual Report Items 421 FF.)

- Eliminate inefficiencies in the statutory health insurance (GKV) without compromising the provision of medically necessary services Item 155

- Retain partial insurance within the social care insurance (SPV) and make it more targeted Item 149

- Increase the labour volume, including through a longer working life, abolition of the joint tax return for married couples and of mini-jobs Item 159

- Strengthening productivity growth through reforms Item 160

- Reform hospital care to promote greater specialisation, clearly verifiable quality standards and reduced reliance on case numbers for funding Items 250 FF.

- Expand outpatient care to avoid the need for inpatient treatment Item 254

- Pricing of innovative medicines should be more closely aligned with therapeutic benefit Item 256

- Higher taxes or minimum prices on tobacco, alcohol and high-sugar foods Items 239 FF.

- Introduce mandatory standards for healthy eating in nurseries and schools; restrict advertising of products that are harmful to health Items 239 FF.

- Increase incentives for second earners by reforming the non-contributory co-insurance scheme for spouses Items 259 F.

- Index-link the federal subsidy for non-contributory benefits Item 258

- Examine the inclusion of civil servants in the GKV Item 263

- Raise thresholds for care assessments to professionally recommended levels Items 339 F.

- Abolish benefits that are not targeted, such as benefit surcharges and relief allowance Items 349 and 342

- Greater use of income and assets to fund care Items 343 FF.

- Targeted support for cases of hardship through means-tested care housing allowance or "help with care" Item 351

- Limit co-payments and make them predictable through the rule-based indexation of SPV benefits Item 352

- Introduce cohort-specific capital funding Items 357 FF.

- Implement a long-term investment strategy with broad international diversification and a higher proportion of equities Items 309 FF.

- Stop contributions to the existing long-term care provision fund and use them to partially finance care for older age groups Item 361

{kind=link}

1. High energy prices weigh on the cyclical recovery

(4) The global economy performed robustly last year, despite the heightened trade policy uncertainty that has persisted for more than a year. During the forecast period, however, protectionist US trade policyITEM 13and the sharp rise in fossil fuel prices resulting from the Iran war ITEM 10are likely to dampen global economic activity. The GCEE expects global gross domestic product (GDP) to grow by 2.3 % in both 2026 and 2027. German exports are therefore likely to increase only weakly over the forecast period. ITEM 57 At the same time, competitive pressure in global markets is increasing. China is increasingly emerging as a competitor in industrial products ITEM 42 and once again increased its goods exports to Europe, the most important sales market for German exports, in 2025.

(5) The German economy is developing weakly. In 2025, economic output barely increased following two years of recession. ITEM 35 Goods exports declined for the third year in a row, ITEM 56 private investment fell, ITEM 52 and manufacturing output stagnated. ITEM 40 The sharp rise in oil prices is likely to lead to a deterioration in Germany’s terms of trade in 2026. ITEMS 39 AND 60 This reduces households’ purchasing power and, consequently, private consumption. Higher production costs are weighing on firms and reducing investment demand. By contrast, public spending financed by the fiscal package adopted in March 2025 will provide support over the forecast period ITEM 45 and boost public civil engineering investment and investment in machinery and equipment. ITEM 53 Leading indicators for private housing construction have also recently pointed to expansion.

(6) The GCEE expects German gross domestic product to rise by 0.5 % in real terms in 2026. CHART K2 It has thus revised its forecast downwards by 0.4 percentage points compared with the GCEE Annual Report 2025. This revision is primarily attributable to the effects of the Iran war. ITEM 10 For 2027, the GCEE expects gross domestic product output growth of 0.8 %. Consumer price inflation is expected to average 3.0 % in 2026 and 2.8 % in 2027. Core inflation is expected to be 2.4 % in 2026 and 2.9 % in 2027. Downside risks to the German gross domestic product forecast stem in particular from the Iran war lasting longer and having more severe consequences than expected.

2. Social insurance under pressure to reform

(7) Social insurance, covering unemployment, accident, statutory pension, statutory health and social long-term care insurance, forms the central pillar of social protection in Germany. It protects households against major life and employment risks. The sum of the contribution rates levied on insured persons' income subject to contributions across all social insurance schemes ("total social insurance contribution rate") amounts to 42.3 % in 2026. This contribution rate is likely to rise substantially in the coming decades as a result of demographic change. Simulations by the GCEE suggest an increase to 45.4 % in 2030. CHART K3 TOP By 2040, the contribution rate rises to 49.7 %. The increase continues thereafter, albeit at a slower pace. ITEM 109

The simulations also show that, over their working lives, younger cohorts will have to spend a significantly higher share of their lifetime labour income on social insurance contributions than older cohorts. ITEM 112 Rising contributions thus, in combination with the current debt-financed fiscal policy, shift burdens onto today’s younger and unborn generations. Against this backdrop, both intergenerational distribution conflicts and the trade-off between an adequate level of benefits and long-term financial sustainability become significantly more acute.

(8) The burden of taxes and social insurance contributions on labour income in Germany is already very high by international standards. Persistently rising social insurance contribution rates widen the wedge between households’ net wages and firms’ labour costs. ITEM 113 For households, this reduces disposable income, dampening private consumption and incentives to work. For firms, labour costs rise, weighing on labour demand and investment. ITEM 140The rising total social insurance contribution rate is therefore expected to dampen gross domestic product by around 0.5 % to 0.9 % by 2035 relative to a scenario in which the contribution rate remains constant. ITEM 142 CHART K3 BOTTOM

(9) To limit the increase in contribution rates, it is essential to slow expenditure growth and stabilise the revenue base. ITEM 144 Reforms should therefore alleviate demographically driven expenditure pressure, particularly in the statutory pension scheme. ITEM 146 Measures that increase labour volume, such as longer working lives, higher labour force participation and stronger incentives to extend working hours, can help to strengthen the revenue side. ITEM 159 Sustainably strengthening the contribution base requires reforms to boost productivity growth. ITEM 160 Expanding the contribution base to include additional types of income, as proposed by some, would be inappropriate for insurance branches with a wage-replacement function. ITEM 151 Non-contributory benefits should be financed from tax revenue if they fulfil clearly justified functions for society as a whole. At the same time, it should be examined whether individual non-contributory benefits are justified. ITEMS 154 F.A Differing Opinion Items 161 FF.

3. Statutory health insurance: curbing rising expenditure, stabilising revenue

(10) The health insurance scheme in Germany is designed to ensure reliable access to medically necessary care and to protect those affected from excessive financial burdens resulting from high treatment costs. Around 90 % of the population are insured under the statutory health insurance. It is financed on a solidarity basis through income-related contributions in a pay-as-you-go system and provides benefits regardless of individual health risk. ITEMS 189 FF. Private health insurance charges income-independent contributions that are calculated on a risk-based criteria and are partly saved to fund higher healthcare costs in old age. ITEMS 203 FF. At 11.7 % of GDP, healthcare expenditure in Germany is among the highest in Europe. ITEM 210 Indicators of healthcare efficiency show that, despite this high level of expenditure, Germany ranks only around the OECD average for key health indicators. ITEM 215

(11) Expenditure in statutory health insurance rose by around 64 % in real terms between 2005 and 2025. ITEM 193 Over the same period, contribution-based revenue increased by only just under 31 % in real terms. To cover expenditure, the average contribution rate for statutory health insurance was therefore raised from 14.2 % to 17.1 % over this period. It is expected to reach 17.5 % in 2026. ITEM 195 The rise in the social insurance contribution rate is therefore largely driven by the increase in the statutory health insurance contribution rate. Under current legislation, the average statutory health insurance contribution rate is expected to rise to 19.8 % by 2040.

The rise in expenditure in statutory health insurance is due, on the one hand, to general economic, social and technological trends. These include demographic ageing, ITEM 217 income growth, ITEM 218 the spread of unhealthy lifestyles, ITEM 219 and medical and technological progress. ITEMS 221 F.On the other hand, institutional factors in the German healthcare system also contribute to this rise, in particular moral hazard effects resulting from comprehensive insurance coverage and limited instruments for managing the provision of benefits. Expenditure on hospital treatment and pharmaceuticals has risen particularly sharply recently. CHART K4

(12) In statutory health insurance, the rise in expenditure should be limited by using the available funds less inefficiently. In the hospital sector, reforms aimed at greater specialisation, clear quality standards and reducing the dependence of funding on case numbers offer considerable potential for reducing inefficiencies. ITEMS 250 FF. In addition, the rise in pharmaceutical expenditure could be dampened by consistently aligning the pricing of innovative medicines with their additional therapeutic benefit. ITEM 256 By contrast, higher general cost-sharing by insured persons is suitable only to a limited extent, as it may also reduce the use of necessary services. ITEMS 244 FF. To mitigate the rise in expenditure in the long term, health prevention in Germany, which is underdeveloped by European standards, should be strengthened through binding standards for healthy nutrition in day-care centres and schools, restrictions on advertising, for example for products harmful to health, and higher taxes or minimum prices on tobacco, alcohol and foods and beverages high in sugar. ITEMS 239 FF.

Reforms to increase revenue can also help stabilise statutory health insurance, but they cannot replace the necessary structural adjustments on the expenditure side. The burden on statutory health insurance arising from non-contributory benefits could be reduced either by increasing federal subsidies or by reducing these benefits. ITEM 258 Abolishing non-contributory co-insurance for spouses who are not raising children could also contribute to this. At the same time, this would increase incentives for second earners to work. ITEMS 259 F. Expanding the contribution base could broaden the revenue base of statutory health insurance, but could also trigger shifts into private health insurance. Including civil servants into the statutory health insurance could strengthen its financing. ITEMS 262 F.

4. Social long-term care insurance: refocusing and ensuring intergenerational equity in financing

(13) The need for long-term care is a fundamental risk. It entails considerable organisational and financial burdens for those affected and their relatives. In Germany, around six million people were in need of long-term care in 2024 according to the definition of social law. ITEMS 281 FF.Long-term care is provided through a mix of informal, outpatient and inpatient care. ITEMS 287 FF. Around 70 % of those in need of care are cared for at home by relatives or outpatient care services. Informal care is provided predominantly by people of working age, and especially by women. ITEM 288

The pay-as-you-go social long-term care insurance scheme was introduced in 1995. It is designed as partial insurance, meaning that it covers part of the costs of long-term care. ITEMS 296 FF. Those in need of care must bear the remaining costs themselves. Owing to wage increases in the care sector, out-of-pocket payments for inpatient care, which affects around 17 % of those in need of care, have risen significantly in recent years. ITEMS 312 FF. These must be financed from income and assets or through private supplementary provision. ITEMS 315 FF. If these resources are insufficient, there is an entitlement to means-tested social assistance in the form of "care allowance". ITEM 320

(14) Expenditure in social long-term care insurance has risen sharply, particularly since 2017. ITEMS 304 FF. This is primarily due to the second long-term care strengthening act, which both simplified access to benefits under social long-term care insurance and expanded the scope of those benefits. CHART K5 TOP The rise in expenditure has subsequently led to higher contribution rates, while demographic ageing has so far contributed only to a limited extent to expenditure growth. In future, however, it is likely to become the main driver. ITEMS 327 FF. As the share of very old people increases, the number of those in need of care rises, and with it the number of benefit recipients. At the same time, the share of people of working age is declining, meaning that contribution-based revenue cannot keep pace to the same extent. This gives rise to a structural financing problem in the pay-as-you-go social long-term care insurance scheme, which is likely to lead to further increases in contribution rates over the long term. ITEM 307

(15) Previous reforms of social long-term care insurance have primarily aimed to improve care provision. Future reforms should make financing more equitable across generations and take account of needs-based care as well as the personal responsibility of those in need of care. In doing so, the trade-off between the scope of benefits, the level of the contribution rate and the level of out-of-pocket payments must be resolved. This cannot be achieved through a single measure; rather, a package of measures is needed.

(16) To limit expenditure growth, access to benefits under social long-term care insurance should be made more restrictive. To this end, the definition of long-term care need, which was revised in 2013, should be reviewed and aligned more closely with expert recommendations. This would reduce the number of people in need of care and, at the same time, lower the average care grade. ITEM 339 In addition, poorly targeted benefits should be reduced. This applies in particular to the benefit supplement for inpatient care ITEMS 349 FF. and to the relief amount, ITEMS 342 FF. which together accounted for around 15 % of total expenditure in social long-term care insurance in 2025. Aligning benefit indexation with cost developments, which are determined largely by wage developments, would stabilize the benefit level over the long term and counteract rising out-of-pocket payments, but it would significantly increase contribution rates. The resulting financial burden would fall primarily on younger generations and would exacerbate intergenerational distribution conflicts. ITEM 112 To stabilize the benefit level of social long-term care insurance and make its financing more equitable across generations, cohort-specific funded provision should therefore be introduced within social long-term care insurance. ITEMS 354 FF. CHART K5 BOTTOM If cohort-specific funded provision is combined with the proposed reforms to dampen expenditure growth, the contribution rate would be stabilised at approximately its current level over the long term. A Differing Opinion Items 363 FF.

HIGH ENERGY PRICES WEIGH ON THE CYCLICAL RECOVERY

- Energy prices have risen sharply as a result of the war in Iran. The increase weighs on the cyclical recovery in Germany and leads to a significant rise in consumer prices.

- GDP growth in Germany will be driven largely by rising public expenditures during the forecast period.

- The GCEE expects Germany's real GDP to grow by 0.5 % in 2026 and 0.8 % in 2027. Consumer price inflation is expected to rise by an annual average of 3.0 % and 2.8 % respectively.

SOCIAL INSURANCE UNDER PRESSURE TO REFORM

- Due to demographic change, under current legislation, the total social insurance contribution rate is expected to rise from the current 42.3 % of income subject to contributions to almost 50 % by 2040.

- An increase in contribution rates reduces the disposable income of private households and increases labour costs for firms. Both factors dampen overall economic growth.

- Stabilising contribution rates could be achieved by limiting expenditure growth and strengthening the revenue base.

STATUTORY HEALTH INSURANCE: CURBING THE RISE IN EXPENDITURE, STABILISING REVENUE

- Despite above-average healthcare expenditure compared to the EU and OECD, Germany achieves only average health outcomes.

- On the expenditure side, statutory health insurance (GKV) contribution rates are driven by demo-graphic ageing, unhealthy consumer behaviour and advances in medical technology, whilst the reve-nue base subject to contributions is growing more slowly.

- To curb future increases in GKV contribution rates, reforms aimed at more effective expenditure control in inpatient care and in the pharmaceutical sector are particularly appropriate.

SOCIAL LONG-TERM CARE INSURANCE: FOCUSING ON PRIORITIES AND ENSURING INTERGENERATIONAL FAIRNESS IN FUNDING

- SPV expenditures have risen sharply since the introduction of the Second Long-Term Care Strengthening Act in 2017. The reasons for this are easier access to and the significant expansion of benefits. Demographic ageing will cause long-term care costs to rise further in the future.

- The SPV should remain a partial insurance scheme. Restricting access to SPV benefits to a level recommended by experts, along with the abolition of the benefit surcharge and the relief allowance, would significantly curb the rise in expenditure.

- In combination with cohort-specific capital funding, such reforms can ensure an appropriate level of benefits with intergenerationally fair financing in the long term.

Your browser is outdated

Please update your Browser to view this website properly.

You will need at least Internet Explorer 11 to see our interactive charts.

Mozilla Firefox

or alternatively Google Chrome

will provide the best experience for this website.

Update your browser now