![[Translate to english:]](/fileadmin/_processed_/4/6/csm_Header_klein_Bild_option4_4b3dd04499.jpg "[Translate to english:]")

Managing the energy crisis in solidarity, shaping the new reality

EXECUTIVE SUMMARY

Click to share

(1) In Spring 2022, Russia initiated a war of aggression against Ukraine, and its consequences pose major economic challenges for Europe, and especially Germany. Energy prices have continued to rise sharply since the start of the war. The substantial reduction in Russian natural gas supplies in the summer of 2022 has exacerbated the energy crisis and fuelled inflation, after it was already elevated in 2021. This is placing a massive burden on households and companies ITEMS 119 FF. AND 314 FF. and significantly clouds the economic outlook. ITEMS 42 FF. AND 66 FF. To make matters worse, the negative economic consequences of the coronavirus pandemic have not yet been fully overcome and supply chain disruptions persist. Together with noticeable shortages of skilled workers in certain occupations, all of these factors are slowing the economic recovery. ITEM 25 FF.

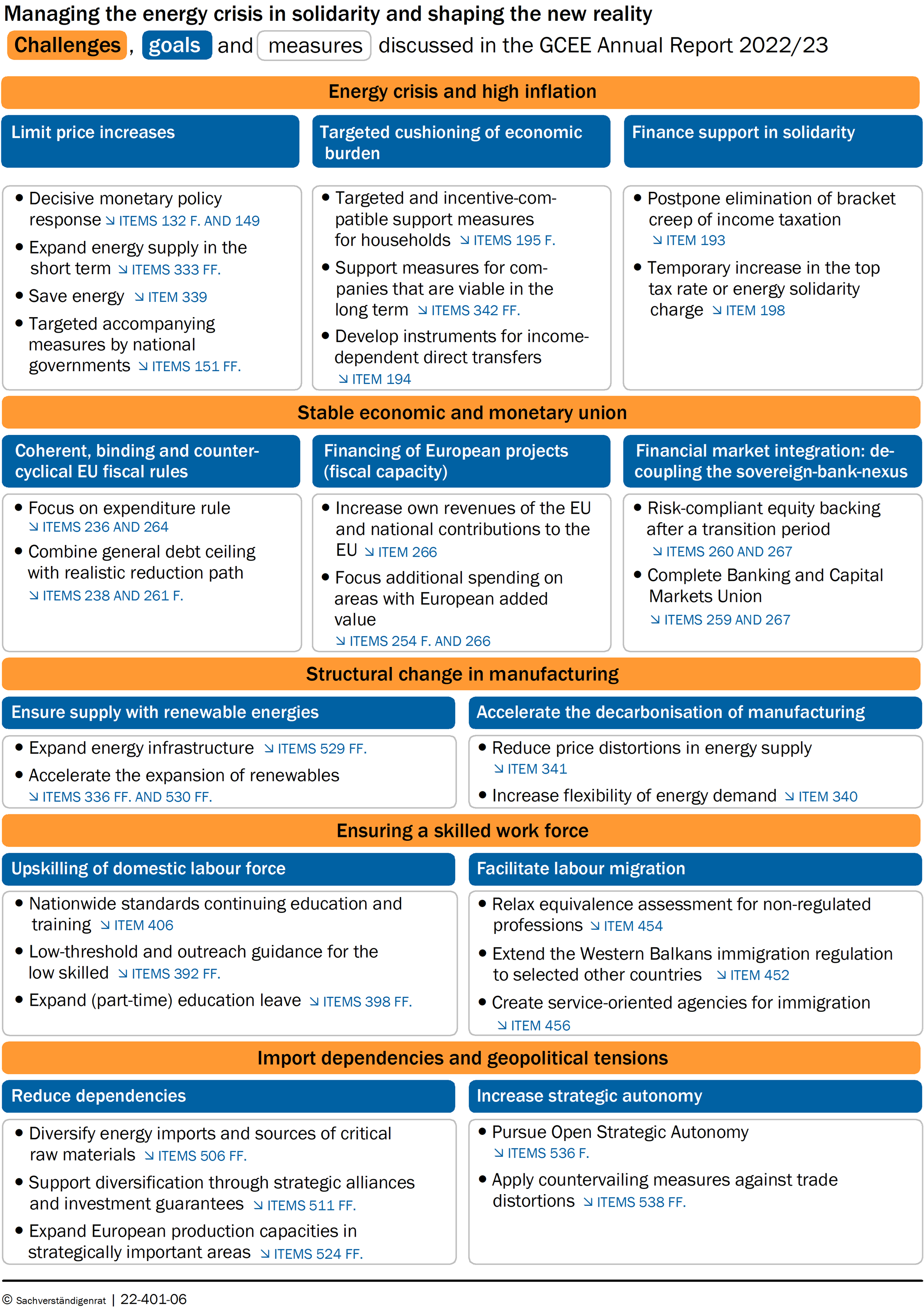

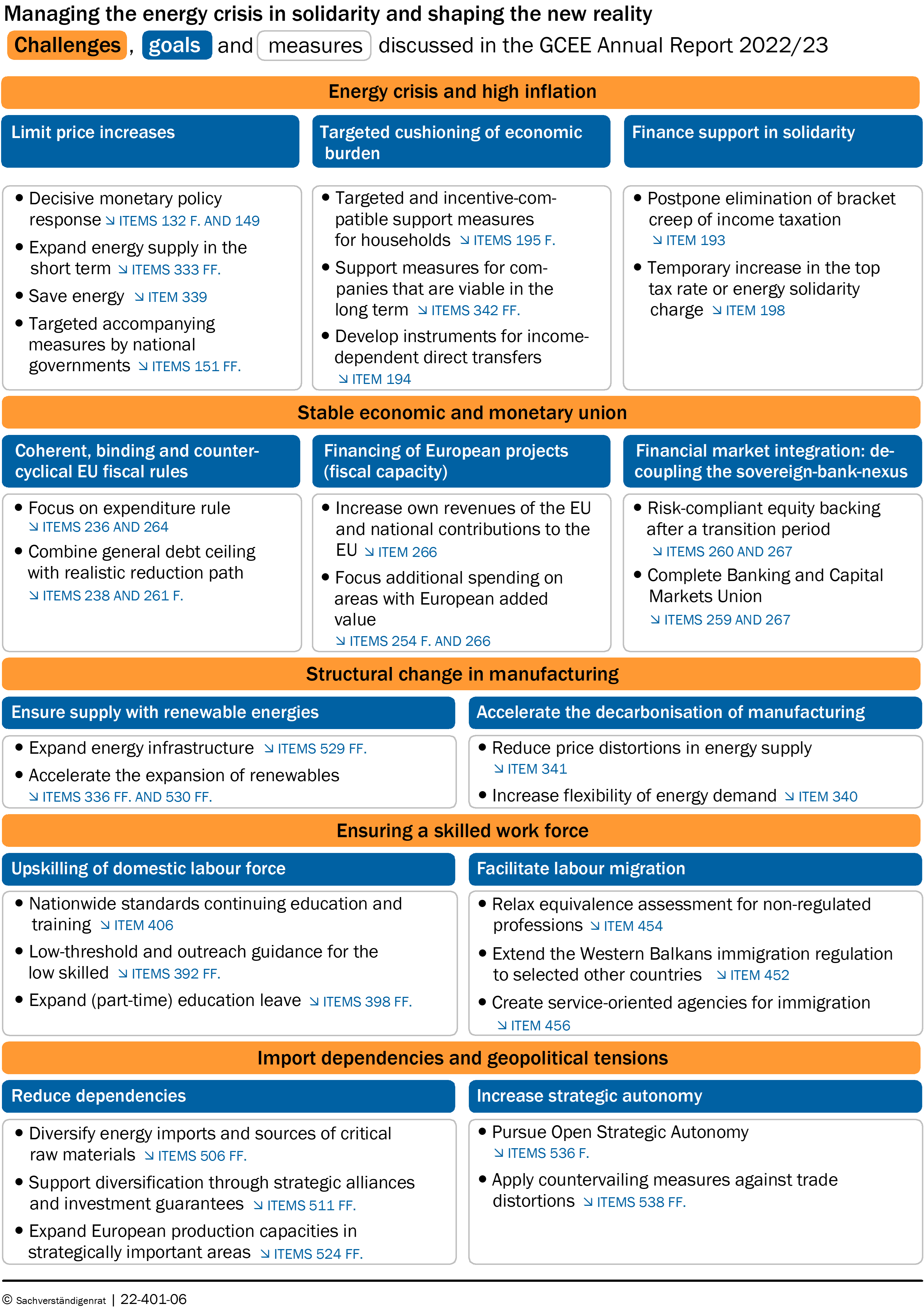

(2) Germany and Europe should manage the energy crisis in solidarity. CHART K1 The crisis requires comprehensive measures to address the energy shortage and provide targeted relief. Strengthened supply and increased energy savings, especially for natural gas, will help manage the energy shortage. ITEMS 333 FF. Relief measures should be targeted along three dimensions. First, they should not weaken the scarcity signal of high energy prices but maintain a strong incentive to save energy. ITEM 195 Secondly, support should, as much as possible, only be provided to those households that are affected by high energy prices and are unable to cope with them, and to those companies that are particularly burdened by high energy prices but have a viable business model in the medium term. ITEMS 193 F. AND 342 FF. Third, relief measures should not put undue strain on government budgets ITEM 197 and, in view of the high inflation rates, should not unduly increase demand and thus price pressure. ITEM 153 In view of the European dimension of the energy crisis, European partner countries should closely coordinate government measures to provide relief and secure energy supplies. ITEMS 48 AND 340

(3) Due to the geopolitical changes and the energy crisis, Germany and Europe face a new reality. This reality must be shaped actively and in close cooperation with the member states of the European Union (EU). CHART K1 It is important not to neglect medium to long-term challenges such as decarbonisation, demographic ageing and the stability of the economic and monetary union. All of this requires a joint approach and solidarity in Europe. In view of high debt-to-GDP ratios and rising interest rates, as well as the crisis-induced increased demands on the fulfilment of government tasks, the institutional framework of the economic and monetary union should be strengthened. ITEMS 218 FF. The loss of Russian energy supplies necessitates the joint procurement of energy and the expansion of the European energy supply, especially of renewable energies. In addition, incentives to increase the energy efficiency of households and companies should be maintained and improved. ITEMS 333 FF. Demographic change is reducing the supply of labour, while structural change is also changing the demand for labour. Against this background, continuing education and training should be improved and labour force migration should be facilitated. ITEMS 355 FF. Last but not least, the increasing influence of geostrategic considerations on international trade poses new challenges for the German economy. Strengthening the resilience of supply chains and securing strategic autonomy should be pursued jointly with EU partners. ITEMS 500 FF.

- Decisive monetary policy response ITEMS 132 F. AND 149

- Expand energy supply in the short term ITEMS 333 FF.

- Save energy ITEM 339

- Targeted accompanying measures by national governments ITEMS 151 FF.

- Targeted and incentive-compatible support measures for households ITEMS 195 F.

- Support measures for companies that are viable in the long term ITEMS 342 FF.

- Develop instruments for income-dependent direct transfers ITEM 194

- Focus on expenditure rule ITEMS 236 AND 264

- Combine general debt ceiling with realistic reduction path ITEMS 238 AND 261 F.

- Increase own revenues of the EU and national contributions to the EU ITEM 266

- Focus additional spending on areas with European added value ITEMS 254 F. AND 266

- Risk-compliant equity backing after a transition period ITEMS 260 AND 267

- Complete Banking and Capital Markets Union ITEMS 259 AND 267

- Expand energy infrastructure ITEMS 529 FF.

- Accelerate the expansion of renewables ITEMS 336 FF. AND 530 FF.

- Nationwide standards for continuing education and training ITEM 406

- Low-threshold and outreach guidance for the low skilled ITEMS 392 FF.

- Expand (part-time) education leave ITEMS 398 FF.

- Diversify energy imports and sources of critical raw materials ITEMS 506 FF.

- Support diversification through strategic alliances and investment guarantees ITEMS 511 FF.

- Expand European production capacities in strategically important areas ITEMS 524 FF.

- Pursue Open Strategic Autonomy ITEMS 536 F.

- Apply countervailing measures against trade distortions ITEMS 538 FF.

{kind=link}

{kind=link}

1. Energy crisis and inflation weigh on the economy

(4) Germany's gross domestic product (GDP) in Q3 2022 slightly exceeded the level from Q4 2019 - before the Corona crisis. ITEM 53 However, the economic outlook in Germany has worsened considerably due to the consequences of the Russian war of aggression against Ukraine. The steep hikes in energy prices have diminished purchasing power and dampen private consumption. They also impair production, especially in energy-intensive industries. High economic uncertainty and weak foreign trade imply that investments and exports are unlikely to stimulate growth in the short term. Supply chain disruptions, however, are expected to gradually decline, al-lowing companies to process their high- level order backlog. Moreover, private households are expected to spend a larger share of their income and savings to smooth consumption. These developments, as well as the robust labour market and the relief packages, especially the gas price brake, should dampen the downturn. The GCEE expects Germany's GDP to grow by 1.7 % in 2022. CHART K2 TOP Growth in 2022 results from the statistical over-hang at the end of 2021 and economic growth during the 1st half of 2022, while stagnation is likely in the second half. In 2023, downward forces are expected to prevail and GDP is expected to decline by 0.2 %. ITEMS 66 FF.

There are significant downside risks to the economic outlook. ITEMS 47 FF. First and foremost, a particularly cold winter in 2022/23 or a further reduction in natural gas supplies could cause energy prices to rise further. In an extreme scenario, a gas shortage could result in widespread production losses and a sharp increase in establishment closures.

(5) In October, consumer price inflation in Germany reached a year-on-year rate of 10.4 %, the highest level since the early 1950s. ITEM 52 Inflation is driven by rising prices in all of the three main components, energy, food and core inflation. CHART K2 BOTTOM For the year ahead, wholesale energy prices are expected to be increasingly passed through to consumer prices for energy and domestic goods and services. Inflation is therefore likely to remain high. In light of the expected wage increases and high import prices for non-energy goods, core inflation is likely to further increase.

However, the upward momentum is likely to slow somewhat over the course of the year. For 2022, the GCEE expects an inflation rate of 8.0 % in Germany. For 2023, inflation is estimated at 7.4 % for Germany. ITEM 71

Decisive reaction by the ECB is appropriate

(6) The burden of the strongly increased inflation differs significantly across private households. One reason is different individual consumption baskets. ITEMS 119 FF. CHART K3 Households in the lower half of the income distribution experience higher individual inflation rates as energy and food make up a higher share of their expenditures. Another reason is that low-income households have to spend a higher share of their net disposable income on current costs of living. In the lowest income decile, more than 60 % of households have a savings rate of less than or equal to zero and thus have very little leeway to keep their consumption constant. Therefore, these households are particularly hard hit. Inflation leads to growth and welfare losses in the overall economy through inefficient use of resources, tax distortions and increased price adjustment costs. ITEM 117 F. The longer high inflation rates persist, the greater the risk that there will be long-term effects on household behaviour. Inflation expectations could then rise, which is likely to have a lasting impact on households' consumption and saving decisions. ITEMS 126 FF.

(7) In addition to the shortage of energy supply, high global demand and supply chain disruptions have been the main drivers of inflation. The negative supply-side shocks are also weighing on the real economy. A restrictive monetary policy to curb inflation is dampening demand and putting additional pressure on the real economy. The European Central Bank (ECB) must nevertheless continue to act decisively to prevent inflation expectations from de-anchoring and to bring inflation back to the target of 2 % in the medium term. ITEM 149 This would help to maintain the ECB’s credibility. The challenge will be to raise interest rates adequately in order to fight inflation without causing an excessive slump in economic activity. Supportive measures by national governments can help dampen the risk of a wage-price spiral. ITEMS 151 FF. However, as these measures also increase demand, they could heighten inflationary pressures and should therefore be targeted as much as possible. ITEMS 154 F.

Targeted cushioning of the impact of high energy prices

(8) In connection with the Russian attack on Ukraine, the price of natural gas in particular has risen steeply since autumn 2021, and its wholesale price has reached new highs in 2022. ITEMS 291 FF. As a result, the costs of electricity production by gas-fired power plants have also strongly increased, leading to significant price increases in the electricity market as well. Some of the price increases have been passed on to private households and industrial customers. Further price increases are likely in the coming year, especially for households. In order to limit the rise in energy prices, the already extensive efforts to procure LNG should be stepped up even further. ITEMS 333 FF. In addition, a more ambitious expansion of renewable energies, a temporary return of coal-fired power plants from the reserve and the planned postponement of the closure of nuclear power plants could ease the situation in energy markets.

(9) Extensive relief measures have been passed to cope with the energy crisis and to cushion its short-term consequences. ITEMS 180 FF. AND 342 FF. These are necessary in view of the enormous price increases. However, it would have been helpful if the necessary plans for relief and energy-saving measures had been prepared much earlier. Ideally, direct transfers would provide targeted relief to those households that are particularly hard hit by high inflation and at the same time have hardly any financial leeway to bear the burdens. An unbureaucratic instrument for income-based direct transfers needs to be developed as quickly as possible. ITEM 194

(10) Past measures to relieve the burden on households, CHART K4 such as the fuel discount, were often poorly targeted and benefited to a large extent the higher income groups. ITEM 193 Taxable one-off payments for all as well as the gas price brake proposed by the Experts’ Commission Gas and Heat are, however, a reasonable solution under the current conditions, as higher income groups have to pay tax on part of the relief. Offsetting the bracket creep in income taxation is fundamentally necessary from the perspective of the tax system. However, the current situation, in which a targeted relief for lower income groups appears to be necessary in the short term and the situation of public finances remains tense, a postponement of this compensation to a later point in time would be appropriate.

(11) For companies, the high energy prices are likely to lead to a temporary reduction in production. Short-time work can help bridge this phase. ITEM 73 In addition, direct support measures could bridge temporary bottlenecks. ITEMS 342 FF. Measures that directly reduce companies' energy costs, such as the electricity and gas price brakes, bring particularly rapid relief. When designing them, it is important to ensure that incentives for energy savings are maintained and that energy costs are not reduced below the price level expected for the long term. Appropriately designed measures would provide incentives for medium-term adjustments, which are necessary in light of the permanent increase in energy prices. It is key that the measures provided are primarily used by those companies whose business model remains viable under these new conditions. Care should be taken to ensure that there are no windfall profits for companies that relocate their production despite support. The proposal of the Experts’ Commission Gas and Heat for the gas price brake would partly fulfil these requirements. ITEMS 345 FF.

(12) The energy crisis strongly affects German public finances. ITEMS 165 FF. High inflation has significantly increased tax revenues. At the same time, the increased prices, the relief measures already adopted, and rising interest rates on government bonds will increase government spending. In 2022, the application of the exception clause of the debt brake provided the leeway necessary for an increase in net borrowing. ITEM 165 This leeway is now being used, among other things, to expand the Economic Stabilisation Fund (ESF), which finance the relief measures of the coming years. On the one hand, from the perspective of budget transparency, the use of the ESF should be viewed critically. ITEM 191 On the other hand, the ESF likely limits the expenditure to be financed with debt to a greater extent, restricting it to energy price relief, than a renewed exemption from the debt brake in 2023. ITEM 192 In order to limit the inflationary effect of the relief measures and the additional burden on the national budget, partial financing through a strictly time-limited increase in the top income tax rate or the introduction of an energy solidarity surcharge for higher earners could be considered. ITEM 198 This would also help improve the targeting of the overall package of relief and burdens and would signal that the energy crisis must be dealt with in a spirit of solidarity.

2. Shaping the new reality: Medium-term challenges for Germany and Europe

(13) The Russian war of aggression and the geopolitical changes are a turning point; Germany and Europe are facing a new reality. In addition to overcoming the urgent challenges of the energy crisis, the many medium-term challenges must be met under new geopolitical conditions. The discussion on reforming the economic and monetary union has gained in importance with increasing risks to the sustainability of public finances. ITEMS 199 FF. In addition, higher energy prices mean that energy- and trade-intensive industries will have to deal with fundamental structural change faster than expected. ITEMS 268 FF. The increasing influence of geostrategic considerations on international trade and economic policy challenges the German economy, as it is strongly integrated into global value chains. ITEMS 462 FF. Last but not least, Germany’s ageing population will exacerbate existing shortages of skilled workers in certain occupations and, without high labour migration, potential labour supply will likely decline. ITEMS 355 FF.

Tackling the reform of the economic and monetary union

(14) Given high debt levels, rising interest rates, necessary relief measures due to the energy crisis, and poor growth prospects, it is important to ensure the sustainability of public finances in Europe. ITEMS 207 FF. At the same time, the state must be able to fulfil its role adequately. This includes macroeconomic stabilisation, the financing of public investments, for example in climate policy, education and digitalisation, as well as the setting of framework conditions with market-based incentives for private investments.

(15) Against this background, there are calls at the European level to reform the EU fiscal rules. ITEMS 226 FF. The purpose of these rules is to ensure the sustainability of public budgets and to make it possible to stabilise the economy as well as to finance future-oriented expenditures. Under their current design, the rules fulfil these objectives only to a limited extent. CHART K5 For example, public debt has increased substantially in many EU member states despite existing fiscal rules. Moreover, EU fiscal rules have been pro-cyclical in the past and have provided little incentive to finance future-oriented spending. A stronger focus on an expenditure rule can counteract these problems and increase the transparency as well as the binding nature of the rules. ITEMS 236 AND 264

(16) A resilient economic and monetary union should go beyond the consideration of fiscal rules. The European Stability Mechanism and the NextGenerationEU recovery fund represent temporary fiscal capacities; i.e., jointly provided funds for times of crisis. They could be complemented by joint European financing of projects that deliver a European added value. ITEMS 254 F. AND 266 As of now, there are no convincing proposals for an incentive-compatible design of a common fiscal capacity to absorb macroeconomic shocks. ITEM 266 Strengthened financial market integration could effectively reduce the interdependence between sovereigns and banks (sovereign-bank nexus). The completion of the Banking and Capital Markets Union, the centralisation of supervision and resolution processes and the risk-compliant equity backing of government bonds can contribute to this. ITEM 267

Energy crisis poses challenges for industry

(17) In the past, German industry has purchased energy at prices similar to those of its international competitors. Last year, however, price increases for energy sources in other regions of the world, especially in the US, were significantly lower than in Europe. ITEMS 291 FF.CHART K6 The asymmetric development of energy prices is likely to persist in the coming years ITEMS 299 FF. and could challenge industrial competitiveness. ITEMS 314 FF. While prices in Europe are expected to fall again in the medium term, they are unlikely to return to pre-crisis levels. Therefore, there is a risk that those energy-intensive industries that compete strongly with companies outside the EU will relocate at least parts of their production. This applies above all to metal production and processing, manufacturing of glass and glassware, ceramics, processing of stones and earths, as well as to particularly energy-intensive products in the chemical industry. ITEMS 321 FF.

(18) An expanded energy supply, which seems realistic in the medium term, could sustainably lower energy prices and reduce cost increases for companies. To this end, LNG and hydrogen imports should be secured, energy infrastructure expanded and energy demand made more flexible. ITEMS 40 F. Accelerating the expansion of renewable energy would significantly contribute to meeting higher future demand for electricity and lowering energy prices while supporting the decarbonisation of industry. ITEMS 336 FF.

(19) The current energy crisis is increasing the pressure on companies to reduce their energy intensity. This will further accelerate the already ongoing structural change in manufacturing. The energy intensity of the German economy has already been declining since the oil price crises of the 1970s. BOX 17 This decline has been driven by two developments: less energy-intensive manufacturing industries have gained slightly in importance, but above all, energy efficiency has increased within various manufacturing industries. ITEMS 309 F. If both the government and businesses choose the right course, Germany is expected to avoid a widespread deindustrialisation. ITEM 273

Securing skilled labour through reskilling and labour migration

(20) The ongoing digitalisation and decarbonisation have increased the need for further training and retraining on the labour market. At the same time, the potential domestic labour supply will shrink significantly in the coming years due to demographic changes. ITEMS 355 FF.CHART K7 This is likely to result in bottlenecks of labour in general, of skilled workers in certain occupations in particular. The developments can jeopardise future economic growth, the sustainability of social security systems, and the transformation towards a climate-neutral economy.

(21)Continuing education and training (CET) play an important role in helping the domestic workforce to meet the changed requirements. ITEMS 369 FF. Retraining and further qualification can prevent job loss due to automation from resulting in rising unemployment. Nationwide standards, for example regarding the quality of offers and partial qualification modules, can support the necessary strengthening of CET. ITEMS 396 AND 406 A better understanding of competences needed in the future and a cooperative exchange, especially between small and medium-sized companies, on successful forms of CET are also helpful. ITEMS 379 F. In addition, CET guidance should be available nationwide and better geared to the needs of low-skilled workers, for example through easily accessible offers and outreach guidance. ITEM 392 A nationwide right to a longer (part-time) education and training leave could help employees threatened by structural change to identify and pursue professional reorientation and retooling at an early stage. ITEM 399

(22) Higher labour migration, especially from non-EU countries, is indispensable to stabilise labour supply. ITEM 412 Until now, restrictive requirements of an equivalence assessment for foreign qualifications have slowed down labour migration from third countries. ITEM 446 The high administrative and time costs to obtain visas can also be prohibitive. ITEM 447 In order to lower the main barrier to immigration, it would make sense to abolish the equivalence assessment for non-regulated occupations. ITEM 454 Instead, a job offer and a minimum period of training or study at recognised educational institutions, combined with strict conditions with respect to the right of residence, could suffice as entry requirements. The Western Balkans regulation created such a pathway for labour migration from the Western Balkan countries. Those who migrated via this route are often qualified and mostly integrate well into the labour market. Increased quotas as well as a permanent establishment and extension of the Western Balkans regulation to selected other countries could facilitate managed labour migration. ITEM 452 This would allow for a concentration of administrative resources on the respective third countries, not least in order to approach interested persons directly. In order to speed up the process and strengthen integration, the tasks of the immigration authorities could be centralised at Länder level. These authorities should set themselves up as service-oriented agencies for immigration. ITEM 456

Reduce international dependencies and strengthen resilience of procurement

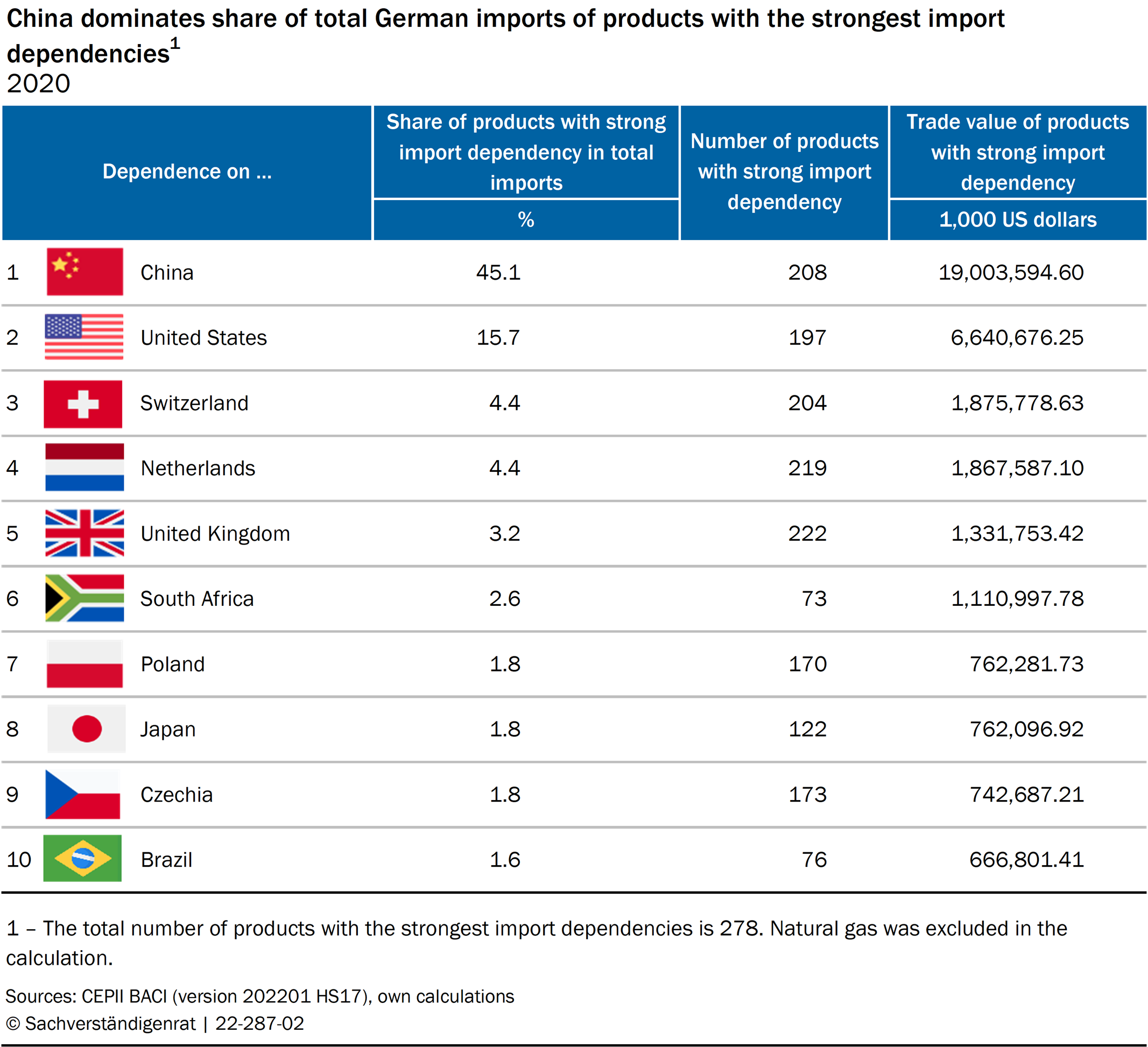

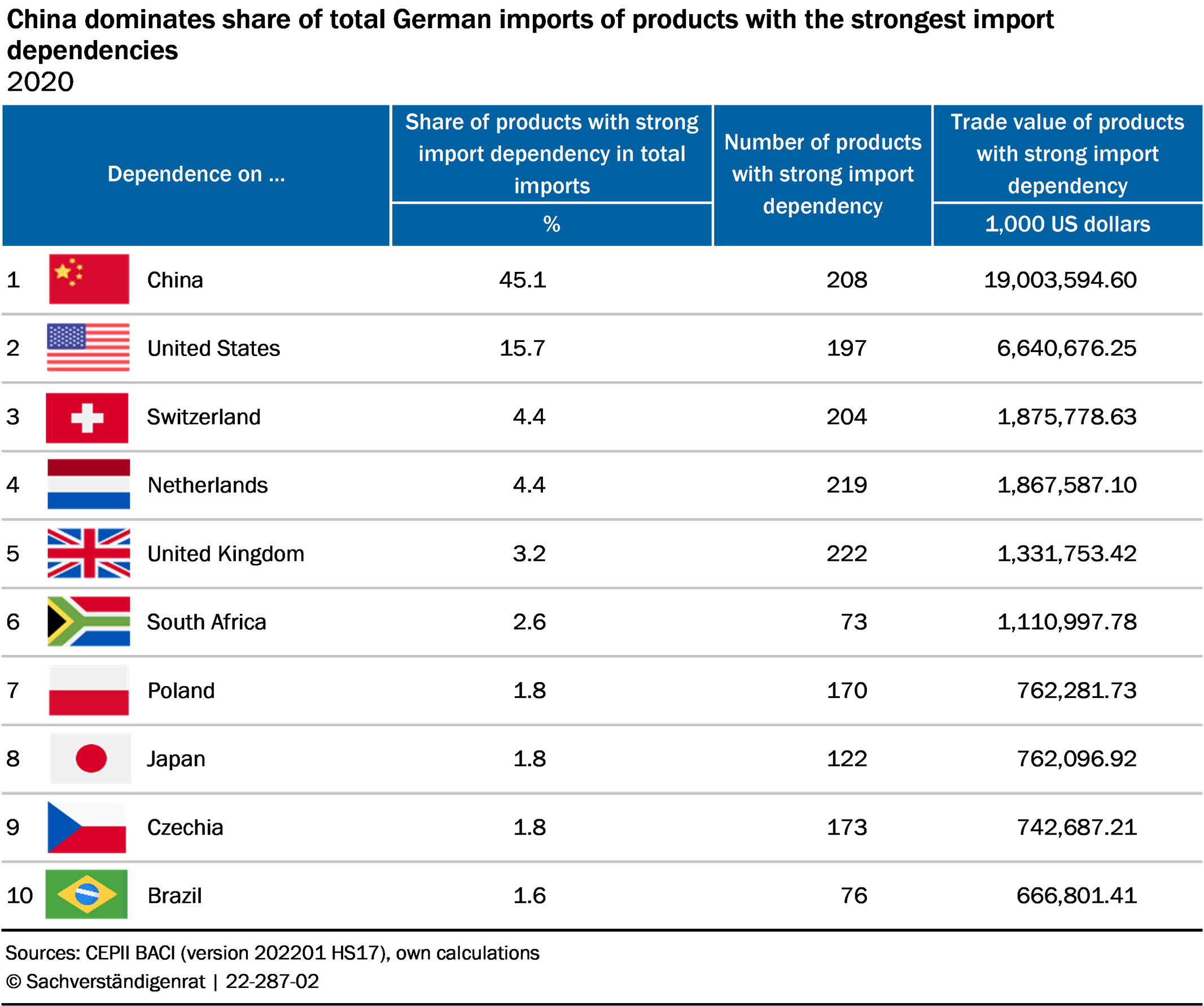

(23) The competitiveness of the German economy relies, to a greater extent than in most large economies, on trade liberalisation and the growing international division of labour. ITEMS 474 FF. Recent crises, however, have revealed the vulnerability of international supply chains and in some cases a high dependence on foreign suppliers. ITEMS 483 F. TABLE K8 In Germany and the EU, dependencies are particularly apparent for energy supply and the supply of critical raw materials. ITEMS 486 FF. In addition, third countries use subsidies in a way that distorts competition, which can render the purchase of critical raw materials and products from other sources uneconomical and create dependencies on these third countries. ITEM 533 F.

(24) In order to avoid dependencies and to increase the resilience of value chains, greater diversification of supply sources is necessary. ITEMS 506 FF. The responsibility for diversification primarily lies with the private sector, but the government can provide targeted support. Strategic alliances, for example in the context of trade agreements, can steer efforts in the right direction. In doing so, the focus should be on countries that share European values and priorities in the areas of democracy, human rights and the rule of law. At the same time, openness towards third countries is important, especially when it comes to providing global public goods such as climate protection or public health. ITEM 509 In addition, the expansion of European production capacities may be appropriate in strategically important areas, such as the development of renewable energies or the domestic extraction of critical raw materials. ITEMS 521 FF. Stockpiling for products of overarching strategic importance could also be facilitated by removing corresponding tax disadvantages.

(25) The geopolitical changes caused by the Russian war of aggression against Ukraine and the tense relationship between the West and China constitute a turning point for Germany and Europe. Given this new reality, European values and interests should be strengthened without diminishing economic openness. The concept of an Open Strategic Autonomy proposed by the European Commission offers a suitable framework for acting as autonomously as necessary, but at the same time as openly as possible. ITEMS 536 FF. Protectionist tendencies as well as trade distorting practices by third party countries should be firmly countered by the EU's expanded trade defence instruments. ITEMS 538 FF.

| Dependence on ... | Share of products with strong import dependency in total imports | Number of products with strong import dependency | Trade value of products with strong import dependency | |

|---|---|---|---|---|

| % | 1,000 US dollars | |||

| 1 |  China China | 45.1 | 208 | 19,003,594.60 |

| 2 |  United States United States | 15.7 | 197 | 6,640,676.25 |

| 3 |  Switzerland Switzerland | 4.4 | 204 | 1,875,778.63 |

| 4 |  Netherlands Netherlands | 4.4 | 219 | 1,867,587.10 |

| 5 |  United Kingdom United Kingdom | 3.2 | 222 | 1,331,753.42 |

| 6 |  South Africa South Africa | 2.6 | 73 | 1,110,997.78 |

| 7 |  Poland Poland | 1.8 | 170 | 762,281.73 |

| 8 |  Japan Japan | 1.8 | 122 | 762,096.92 |

| 9 |  Czechia Czechia | 1.8 | 173 | 742,687.21 |

| 10 |  Brazil Brazil | 1.6 | 76 | 666,801.41 |

{kind=link}

{kind=link}

ECONOMIC OUTLOOK MASSIVELY BURDENED BY ENERGY CRISIS

- High energy prices reduce purchasing power and weigh on private consumption. A stable labour market and easing supply bottlenecks are supporting the economy.

- The GCEE expects real gross domestic product in Germany to increase by 1.7 % this year and to decline 0.2 % in 2023. For consumer price inflation, it forecasts rates of 8.0 % and 7.4 % respectively.

- The forecast is subject to considerable downside risks. Should a shortage of natural gas occur in Germany, a deep recession and even higher inflation can be expected.

INFLATION AND MONETARY POLICY

- Inflation in the euro area has reached its highest level since the inception of the monetary union and is likely to remain elevated for some time. In 2021 it was mainly driven by supply shortages and energy prices, but prices are now rising across the board.

- High inflation leads to welfare losses and has significant distributional effects. Low-income households bear the greatest financial burden owing to their high consumption rates.

- Despite the challenges posed by supply shocks, it is necessary for the European Central Bank (ECB) to maintain its firm response to high inflation for the time being.

GERMAN FISCAL POLICY FACES DIFFICULT CHALLENGES

- Fiscal policy faces another major challenge after the pandemic due to the Ukraine war and the energy crisis. So far, however, the medium-term debt sustainability is not endangered by the necessary additional government borrowing.

- All relief measures should be as targeted as possible. They should include energy saving incentives and be focused on lower and middle incomes.

- A temporary financial participation of those who can shoulder the high prices could reduce the fiscal burden and limit the inflationary effect.

REFORM PERSPECTIVES FOR EUROPEAN FISCAL POLICY

- The Coronavirus pandemic and the Russian war against Ukraine put pressure on national public budgets and exacerbate the tension between debt sustainability and public task fulfilment.

- A binding expenditure rule could make the EU fiscal rules more verifiable, limit risks for debt sustainability, have a stabilising effect on the economy and expand the scope for investment.

- Reforms should go beyond the design of fiscal rules to enable possible financing of joint European projects and a stable financial market.

ENERGY CRISIS AND STRUCTURAL CHANGE: PROSPECTS FOR GERMAN INDUSTRY

- Energy prices are likely to fall again in Europe in the medium term, but are not expected to return to pre-crisis levels. Energy-intensive industries facing strong competition from non-European competitors are particularly affected.

- This will accelerate the structural change in industry that is already expected as a result of decarbonisation, but it is unlikely to lead to broad-based deindustrialisation.

- State support should target companies with sustainable business models and not seek to maintain the status quo. The expansion of renewable energies should be stepped up.

SECURING SKILLED LABOUR: OPTIONS FOR ACTION IN CONTINUING EDUCATION AND LABOUR MIGRATION

- The labour force potential will decline sharply in the coming years due to demographic ageing. Together with structural change, this will exacerbate shortages of skilled workers.

- Targeted and active guidance, standards, modularised courses and an understanding of future competences are needed to strengthen continuing education.

- The necessary labour migration will require a more transparent immigration law, a relaxation of the equivalence assessment relating to the recognition of professional qualifications, and an extension of the Western Balkans Regulation to selected third countries.

COMPETITIVENESS IN TIMES OF GEOPOLITICAL CHANGE

- The competitiveness and, hence also, the success of the German economy over the past few decades have largely been based on its increasing integration into the global economy.

- Economic dependencies and growing geopolitical tensions pose new challenges for Germany and Europe.

- Greater diversification of supply chains, the expansion of European production capacities and infrastructures as well as the strengthening of strategic autonomy are therefore urgently needed.

Your browser is outdated

Please update your Browser to view this website properly.

You will need at least Internet Explorer 11 to see our interactive charts.

Mozilla Firefox

or alternatively Google Chrome

will provide the best experience for this website.

Update your browser now